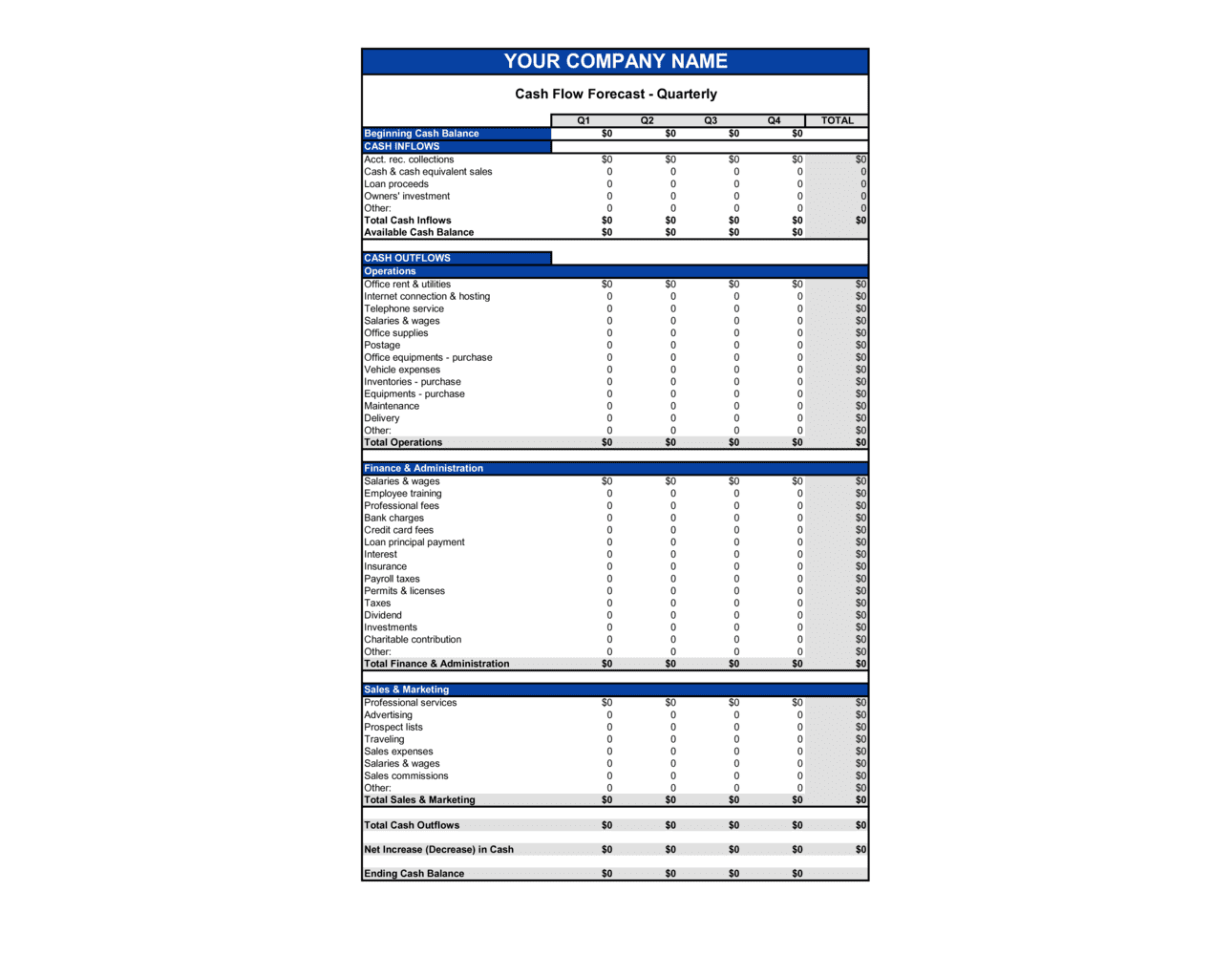

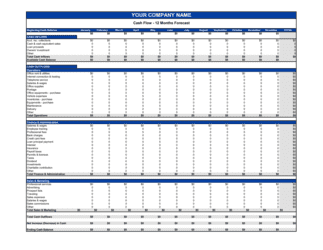

- Opening Cash Balance

- The actual cash and cash-equivalent balance at the start of a forecast period, carried forward from the prior period's closing balance.

- Cash Inflow

- Any receipt of cash into the business during the period — from customer payments, loan proceeds, asset sales, or investment contributions.

- Cash Outflow

- Any payment of cash out of the business — including payroll, supplier invoices, rent, loan repayments, and tax remittances.

- Net Cash Position

- Opening cash balance plus total inflows minus total outflows for the period — the single number that shows whether the business generated or consumed cash.

- Operating Activities

- Cash flows directly tied to the core business — collecting from customers, paying suppliers, and covering operating expenses like wages and rent.

- Capital Expenditure (CapEx)

- Cash spent on acquiring or upgrading long-term assets such as equipment, vehicles, or leasehold improvements — recorded separately from operating outflows.

- Financing Activities

- Cash flows from borrowing or repaying debt, issuing equity, or paying dividends — distinct from operating and investing activities.

- Variance

- The difference between a forecast figure and the actual result for the same period, used to evaluate forecast accuracy and adjust future assumptions.

- Covenant

- A contractual condition in a loan agreement requiring the borrower to maintain specific financial ratios or reporting obligations — often including regular cash flow forecasts.

- Runway

- The number of months a business can continue operating at its current burn rate before its cash balance reaches zero, assuming no new revenue or funding.

- Burn Rate

- The average monthly net cash outflow for a business that is spending more than it earns — typically used to describe pre-revenue or growth-stage companies.

- Accrual vs. Cash Basis

- Accrual accounting records revenue and expenses when earned or incurred; cash basis records them only when cash actually moves — a forecast must specify which basis it uses.