1

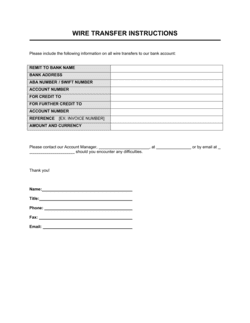

Enter your account holder details and date

Add your full legal name or registered company name exactly as it appears on the bank account, along with your address and today's date. Address the letter to the bank's wire transfer department rather than a general branch address.

💡 Call your bank's wire desk to confirm the correct department address and any specific formatting requirements before submitting.

2

Specify the debit account in full

Enter the full account number (not masked), account type, and the account holder name. If your bank requires a sort code or transit number in addition to the account number, include it here.

💡 Cross-check the account number against a recent bank statement before submitting — a single transposed digit routes the debit to the wrong account.

3

State the exact transfer amount and currency

Write the amount numerically and in words, and include the three-letter ISO currency code (USD, EUR, GBP, CAD). For foreign-currency transfers, confirm with your bank whether the amount is fixed in the foreign currency or you are providing a USD equivalent.

💡 If you need the beneficiary to receive an exact amount net of fees, instruct OUR charges so the full amount arrives intact.

4

Complete the beneficiary details precisely

Enter the beneficiary's full registered name and account number. For international transfers, include the IBAN where required and the full beneficiary address — some correspondent banks reject transfers without a complete beneficiary address.

💡 Ask the beneficiary to send you a pre-filled wire instruction sheet from their own bank rather than relying on a verbal exchange of account numbers.

5

Add the beneficiary bank's routing identifiers

For domestic US transfers, include the 9-digit ABA routing number. For international transfers, include the SWIFT/BIC code and IBAN if applicable. Add the beneficiary bank's full name and address.

💡 Verify the SWIFT code at swift.com/bic-search — an outdated or incorrect code is one of the most common reasons international wires are returned.

6

Include intermediary bank details if instructed

Only add an intermediary bank if the beneficiary's bank or the beneficiary themselves has provided one. Copy the intermediary's SWIFT code and routing number exactly from their written instruction.

💡 Never guess an intermediary bank. If you are unsure, leave the field blank and let your bank determine the correspondent routing.

7

State the purpose of payment clearly

Write a specific one-line description referencing the invoice number, contract, or transaction type. This satisfies AML screening and helps the beneficiary match the payment in their accounts receivable.

💡 For recurring vendor payments, include the invoice number and period (e.g., 'INV-2026-047, April services') rather than a generic label each time.

8

Sign, add your callback number, and submit

An authorized signatory must sign the letter. Include a direct callback phone number where the bank can reach you for verbal verification. Submit via your bank's secure document channel, branch drop-off, or authenticated online portal.

💡 Submit early in the business day — wire cut-off times for same-day value are typically 3:00–5:00 p.m. local time for the sending bank.