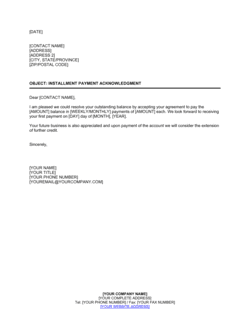

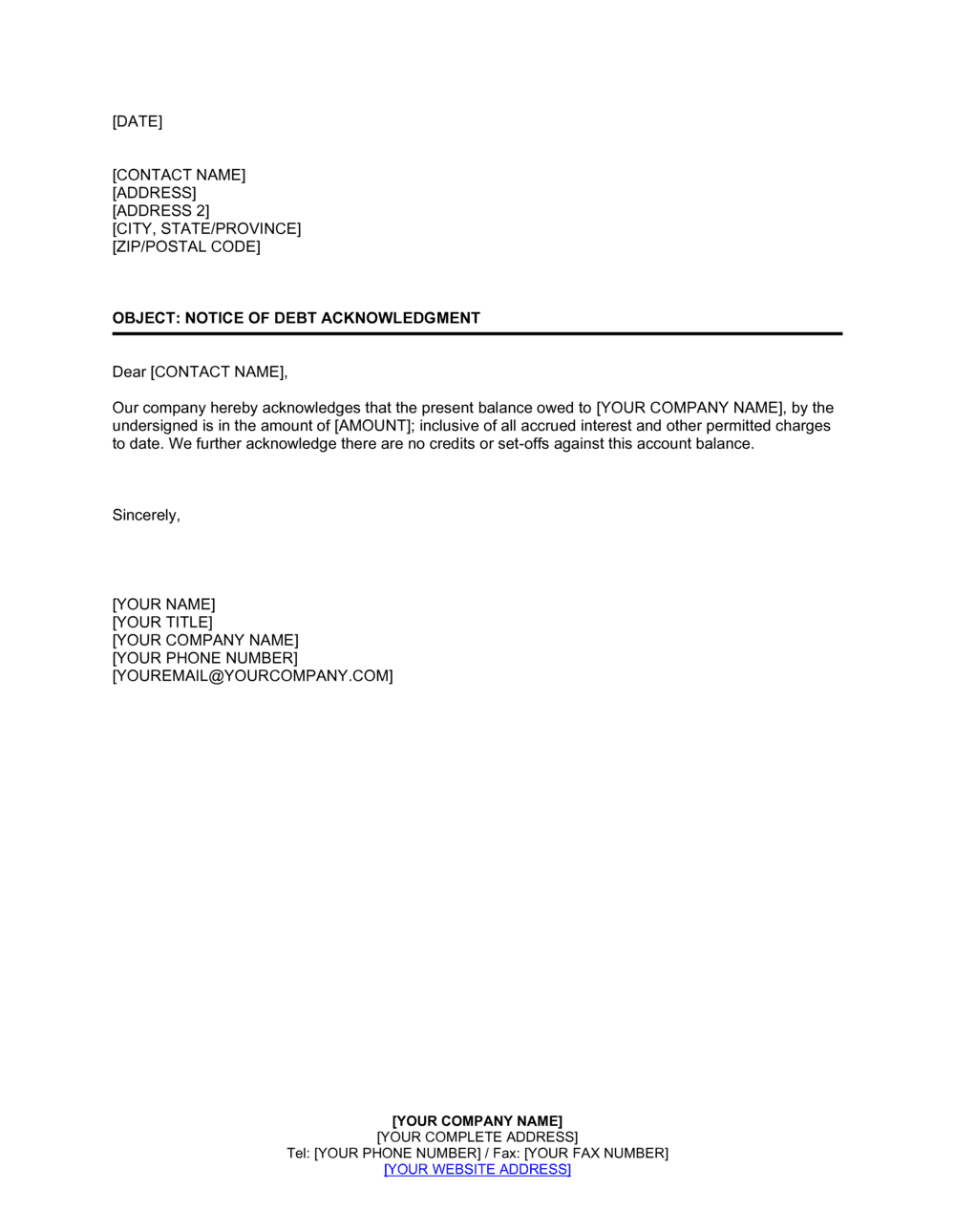

❌ Using hedging or conditional language in the acknowledgment

Why it matters: Phrases like 'I believe I owe' or 'approximately' may not meet the written-acknowledgment standard that resets the statute of limitations, defeating one of the letter's primary purposes.

Fix: State the amount and obligation in definitive terms. Use 'I acknowledge that I owe' followed by the exact figure and a clear description of the debt's origin.