1

Identify both parties using legal entity names

Enter the full registered legal names of both the seller and the buyer. For companies, use the name on the corporate registry, not a trade name or brand name.

💡 Cross-reference the party names against the original sale-on-approval agreement to confirm they match exactly — a name discrepancy can complicate enforceability.

2

Reference the original approval agreement

Enter the date and reference number of the original sale-on-approval or delivery note. This links the return document to the underlying transaction and simplifies accounting reconciliation.

💡 If no formal approval agreement exists, reference the original delivery note or purchase order number instead and note the trial terms that were communicated.

3

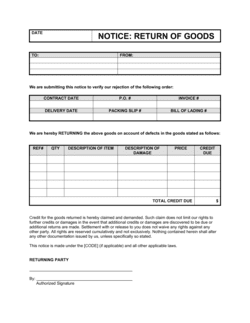

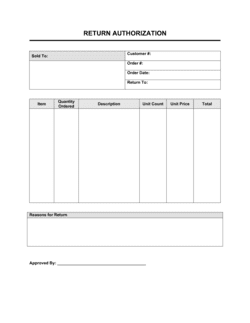

Itemize the returned goods precisely

List every item being returned with its product name, SKU or serial number, quantity, and per-unit value. Confirm the total value of goods being returned.

💡 Match the itemization exactly to the original delivery record — any discrepancy between what was sent and what is listed as returned should be flagged in Schedule A.

4

Document the condition of the goods

State the condition of each returned item. If goods are in original, unopened condition, say so explicitly. If there is any wear, damage, or deviation from original condition, describe it in Schedule A and attach photographs if possible.

💡 Photographs taken at the time of packaging for return shipping are the single most useful piece of evidence in any condition dispute.

5

Set the inspection window and acceptance process

Enter the number of business days the seller has to inspect the goods after receipt. Include what constitutes a valid objection and the consequence of missing the deadline.

💡 Five business days is a practical standard for most goods; extend to ten for complex machinery or high-value equipment requiring specialist inspection.

6

Allocate transit risk and specify shipping instructions

Decide whether buyer or seller bears the risk of loss during return transit and enter the seller's return address and return authorization number format.

💡 For high-value goods, require the buyer to obtain carrier insurance covering the full declared value of the shipment and name the seller as an additional insured.

7

Specify the credit or refund amount and timeline

Enter the exact dollar amount of the credit or refund and the number of business days after return acceptance within which the seller must issue it.

💡 If the credit will be applied to a future order rather than paid out, specify the expiry date of the credit note to prevent it from sitting unresolved on both parties' books indefinitely.

8

Sign before the goods are shipped back

Both parties should sign the return document before the goods leave the buyer's premises. This ensures the agreed condition record and release terms are in place before any transit damage dispute arises.

💡 Use a timestamped eSign solution so the execution date is independently verifiable — particularly important if the approval period expiry date is in dispute.