1

Identify both parties with full legal names and addresses

Enter the seller's and buyer's complete legal names — registered entity names for businesses, not trade names — and their current addresses. For companies, include the jurisdiction of incorporation.

💡 For high-value assets, verify the buyer's legal name against a government-issued ID or corporate registry extract before signing to avoid disputes about which party is bound.

2

Describe the asset precisely

Include every identifying detail: for vehicles, the VIN, make, model, year, color, and odometer reading; for equipment, the manufacturer, model number, and serial number; for other goods, a description specific enough to distinguish this item from similar ones.

💡 Attach photographs of the asset taken on the signing date as a schedule to the agreement — this protects both parties in a condition dispute at repossession.

3

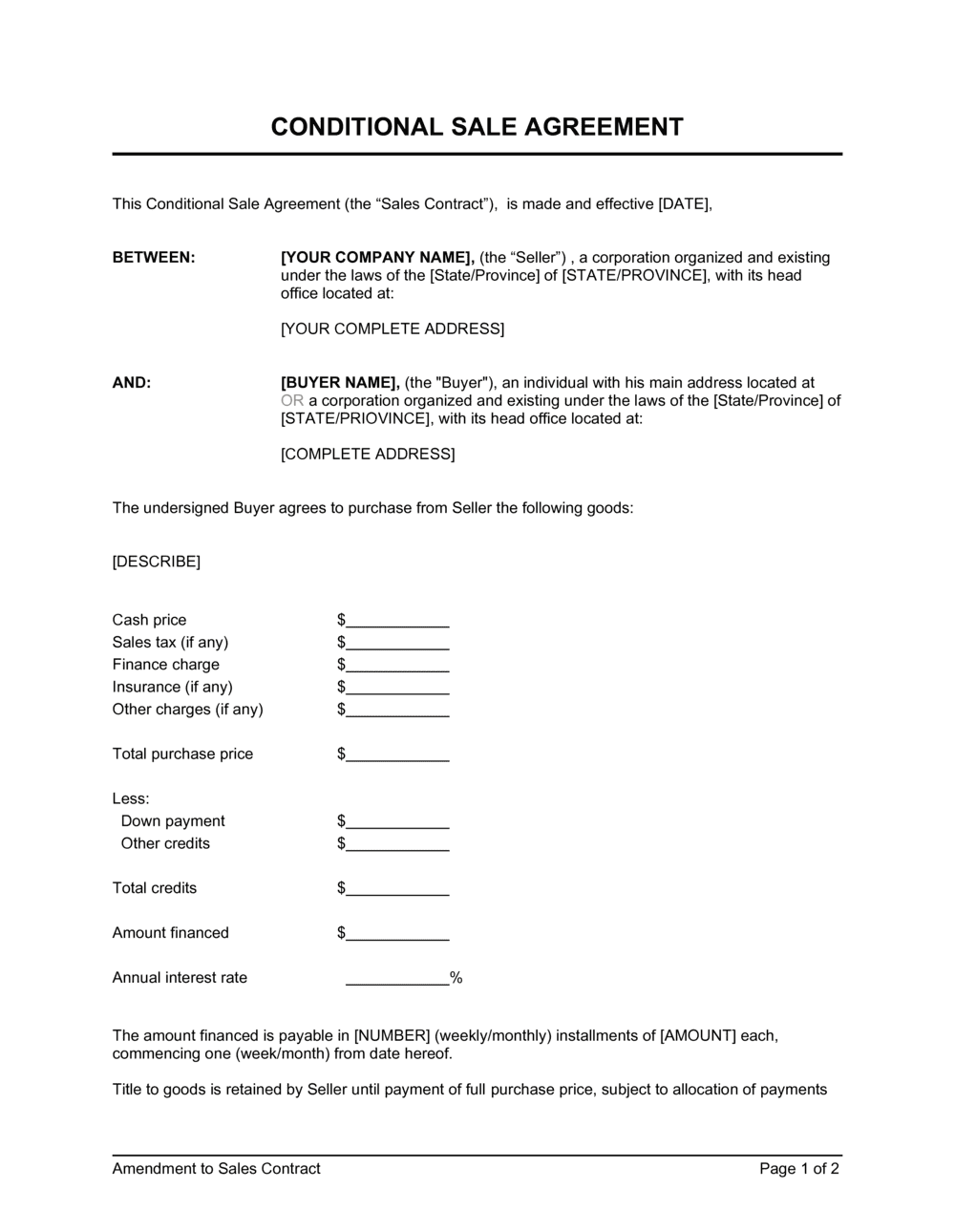

Set the purchase price, deposit, and installment schedule

Enter the total purchase price, the deposit payable at signing, the number of installments, each installment amount, the due dates, and the accepted payment method with full account or remittance details.

💡 Build the installment schedule as a numbered table in a Schedule A rather than prose — it is easier for both parties to track and for a court to interpret if disputed.

4

Draft the title retention and risk-of-loss clauses

Confirm that legal title stays with the seller until final payment, that the buyer holds the asset as bailee, and that risk of loss transfers to the buyer on delivery. Ensure the insurance clause names the seller as loss payee.

💡 In the US, file a UCC-1 financing statement with the appropriate Secretary of State to perfect your retained security interest within 20 days of the buyer taking possession — earlier is better.

5

Define default events and the cure period

List every act that constitutes default — missed payments, unauthorized transfer, insolvency, or breach of use restrictions. Set a cure period that meets or exceeds the statutory minimum in the governing jurisdiction.

💡 Research the statutory minimum cure period in the buyer's state or province before finalizing this clause. Defaulting to '10 days' may be shorter than local law requires for consumer transactions.

6

State repossession rights and the deficiency claim process

Describe the seller's repossession rights on uncured default, the process for selling the repossessed asset, how proceeds are applied, and the buyer's liability for any remaining deficiency.

💡 Check whether the governing jurisdiction requires a specific redemption period — a window during which the buyer can reclaim the asset by paying the full outstanding balance — before the seller may sell it.

7

Confirm governing law and sign before delivery

Choose the governing law of the jurisdiction where the asset will be located and used. Both parties must sign before the asset is delivered — post-delivery signatures create consideration issues under common-law rules.

💡 Use a witness or notary where required by local law — some jurisdictions require witnessed signatures on secured-transaction documents for them to be registered.

8

Attach a bill of sale draft for final title transfer

Include a draft Bill of Sale as Schedule B, pre-signed in escrow or held by the seller, to be released to the buyer upon confirmation of the final payment. This avoids delays in title delivery after the buyer has paid in full.

💡 State in the agreement that the seller will deliver the executed Bill of Sale within five business days of final payment — a specific deadline prevents the seller from delaying title transfer after receiving all funds.