1

Gather your original stop payment documentation

Locate the original stop payment confirmation from your bank, which should include the stop payment date, check number, amount, and payee. You will need these exact details to complete the cancellation form accurately.

💡 Cross-reference your bank's records online or by phone before filling in the form — even a one-digit difference in the check number can cause the cancellation to be misapplied.

2

Enter your account holder and bank details

Complete the account holder identification block with your full legal name or registered business name, address, and contact information. Then enter your bank name, branch address, and full account number.

💡 Use the exact name on file with the bank — not a DBA or abbreviated name — to prevent processing delays.

3

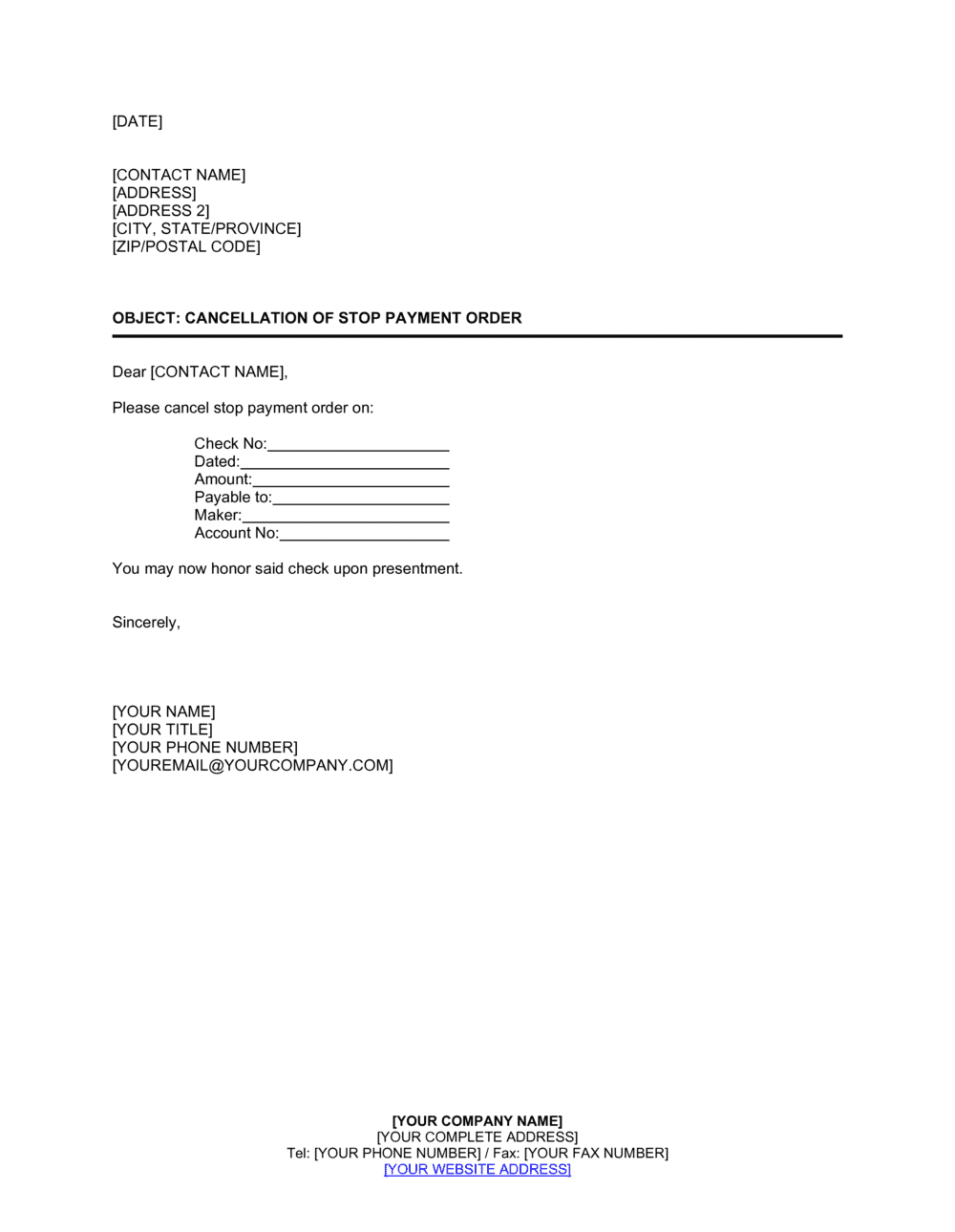

Identify the original stop payment precisely

Fill in the check number, exact dollar amount, payee name, and the date the stop payment was originally placed. All four identifiers should match your bank's stop payment record.

💡 If you are unsure of the exact stop payment date, call your bank's customer service line and request a stop payment history report before submitting.

4

Draft the authorization to honor the instrument

Complete the authorization clause directing the bank to lift the stop payment and honor the check upon its next presentation. Confirm that the account will have sufficient funds to cover the payment on or before the anticipated presentation date.

💡 If funds may be tight on the expected presentation date, coordinate with the payee on timing before submitting the cancellation.

5

Add the reason for cancellation

Briefly state why the stop payment is being revoked — resolved dispute, confirmed delivery of goods or services, or mutual agreement with the payee. Even a single sentence creates a useful audit trail.

💡 Keep the reason factual and neutral — this document may be reviewed by a bank compliance officer or introduced as evidence in a future dispute.

6

Review the hold harmless and fee acknowledgment clauses

Read the indemnification language carefully before signing. Confirm the fee amount listed matches your bank's current fee schedule, and verify that you are comfortable releasing the bank from liability for good-faith processing.

💡 Call your bank to confirm the current cancellation fee before inserting the amount — fees change and an incorrect figure may require a corrected submission.

7

Sign, date, and submit to the bank

Execute the form with a wet or electronic signature matching the bank's account authorization requirements. For joint accounts, obtain all required co-signatures. Submit the form in person, by secure mail, or through the bank's secure document portal.

💡 Request a written confirmation receipt or bank-stamped copy of the cancellation — this is your proof of submission if the bank fails to lift the stop payment in time.

8

Confirm the cancellation was processed

Follow up with your bank within one to two business days to confirm the stop payment has been removed from their system and the check will be honored on presentation.

💡 Note the name of the bank representative who confirms processing and retain that record alongside your submitted cancellation form.