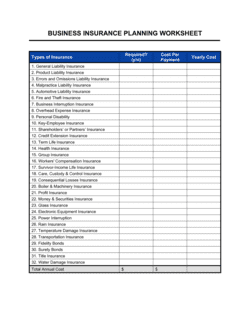

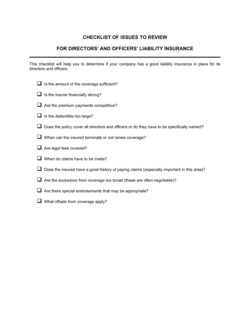

- General Liability Insurance

- Coverage that protects a business against third-party claims of bodily injury, property damage, and personal injury arising from business operations.

- Deductible

- The amount a business pays out of pocket before the insurance policy begins covering a loss.

- Coverage Limit

- The maximum dollar amount an insurer will pay for a covered claim under a given policy.

- Premium

- The periodic payment — monthly or annual — a business makes to maintain an insurance policy.

- Business Owner's Policy (BOP)

- A bundled policy combining general liability and commercial property coverage, typically offered at a lower combined premium than purchasing each separately.

- Errors and Omissions (E&O)

- Professional liability insurance that covers claims arising from mistakes, negligence, or failure to deliver promised services — common for consultants, agencies, and professional service firms.

- Workers' Compensation

- Mandatory coverage in most jurisdictions that pays medical expenses and lost wages for employees injured on the job, in exchange for limiting the employer's tort liability.

- Umbrella Policy

- Excess liability coverage that activates after the limits of an underlying policy are exhausted, providing an additional layer of protection for large claims.

- Certificate of Insurance (COI)

- A one-page document issued by an insurer summarizing a business's active coverage types, limits, and policy periods — commonly required by clients, landlords, and lenders.

- Endorsement

- A written amendment that modifies the terms, coverage, or exclusions of an existing insurance policy.

- Exclusion

- A specific condition, circumstance, or type of loss explicitly not covered by an insurance policy.

- Renewal Date

- The date on which a policy expires and must be renewed or replaced to maintain continuous coverage.