1

Identify the parties and assign a policy number

Enter the insurer's full legal name and jurisdiction of incorporation, the insured's registered legal entity name, and a unique policy number. Confirm the insured name matches the entity that will suffer the loss.

💡 If multiple related entities need coverage, list them separately or use an 'Insured Entities' schedule rather than relying on a general 'affiliates' reference, which courts interpret inconsistently.

2

Define the coverage type and triggering events precisely

Choose the coverage category (general liability, property, professional indemnity, D&O, etc.) and write out the specific triggering conditions — the events that activate the insurer's payment obligation. Avoid relying on the coverage category name alone.

💡 Cross-reference the coverage definition against the exclusions clause before finalizing — the two clauses are often drafted independently and can leave unintended gaps.

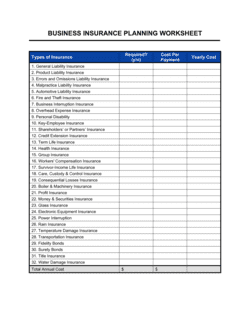

3

Set coverage limits, sublimits, and deductibles

Enter the per-occurrence limit, aggregate limit, and any sublimits for specific loss categories. State the deductible amount and confirm whether it operates as a standard deductible or a self-insured retention.

💡 Run a scenario analysis: if your single largest foreseeable loss (e.g., a complete facility destruction or a class-action claim) hit today, would the per-occurrence limit and sublimits actually cover it?

4

List all exclusions explicitly

Populate the exclusions clause with the standard exclusions for your coverage type plus any negotiated carve-outs. Each exclusion should be specific enough that a claims adjuster can apply it without judgment calls.

💡 Ask the insurer for a list of the top ten claims they have denied under similar policies in the past three years — this tells you which exclusions are actively used and which are theoretical.

5

Set the premium, payment schedule, and grace period

Enter the annual premium, installment due dates, and the number of days in the grace period before coverage lapses for non-payment. Confirm that the grace period meets any statutory minimum in the governing jurisdiction.

💡 Calendar all premium due dates and set reminders 10 business days in advance — a missed payment that lapses coverage on the day of a loss is one of the most costly and avoidable insurance errors.

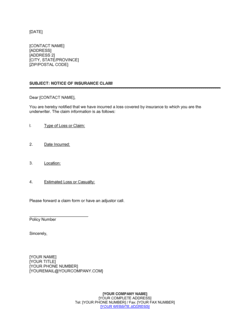

6

Draft the claims notification procedure

Specify the notice period (e.g., 30 days from first awareness), the method (written, to a named claims contact), and the minimum information required in the notice. Include a backup contact in case the primary is unavailable.

💡 In claims-made policies, late notice is a coverage-defeating condition — consider setting your internal notice trigger 10 days earlier than the contractual deadline to create a buffer.

7

Address subrogation waivers if required by related contracts

Review any service contracts, leases, or construction agreements that require a mutual waiver of subrogation. If waivers are needed, add an endorsement to the policy before the contract is signed — not after a loss occurs.

💡 Inform your insurer of any waiver-of-subrogation obligations in writing and get written confirmation that coverage is not affected — verbal assurances from brokers are not binding on the insurer.

8

Execute the agreement before the policy period starts

Both parties should sign before the coverage start date. Attach all schedules (coverage schedule, premium schedule, endorsements) as executed exhibits. Retain the fully executed original in your risk management files.

💡 Request a certified copy of the executed policy from the insurer within 30 days of signing — disputes about what was agreed often arise when parties are working from different versions of the document.