1

Define the scope: one product, one period

Enter the company name, the specific product or service being analyzed, and the time period — typically one month or one year. If you sell multiple products, run a separate analysis for each.

💡 Use a monthly analysis when costs and revenues fluctuate seasonally; use an annual analysis for stable businesses applying for a bank loan.

2

List every fixed cost for the period

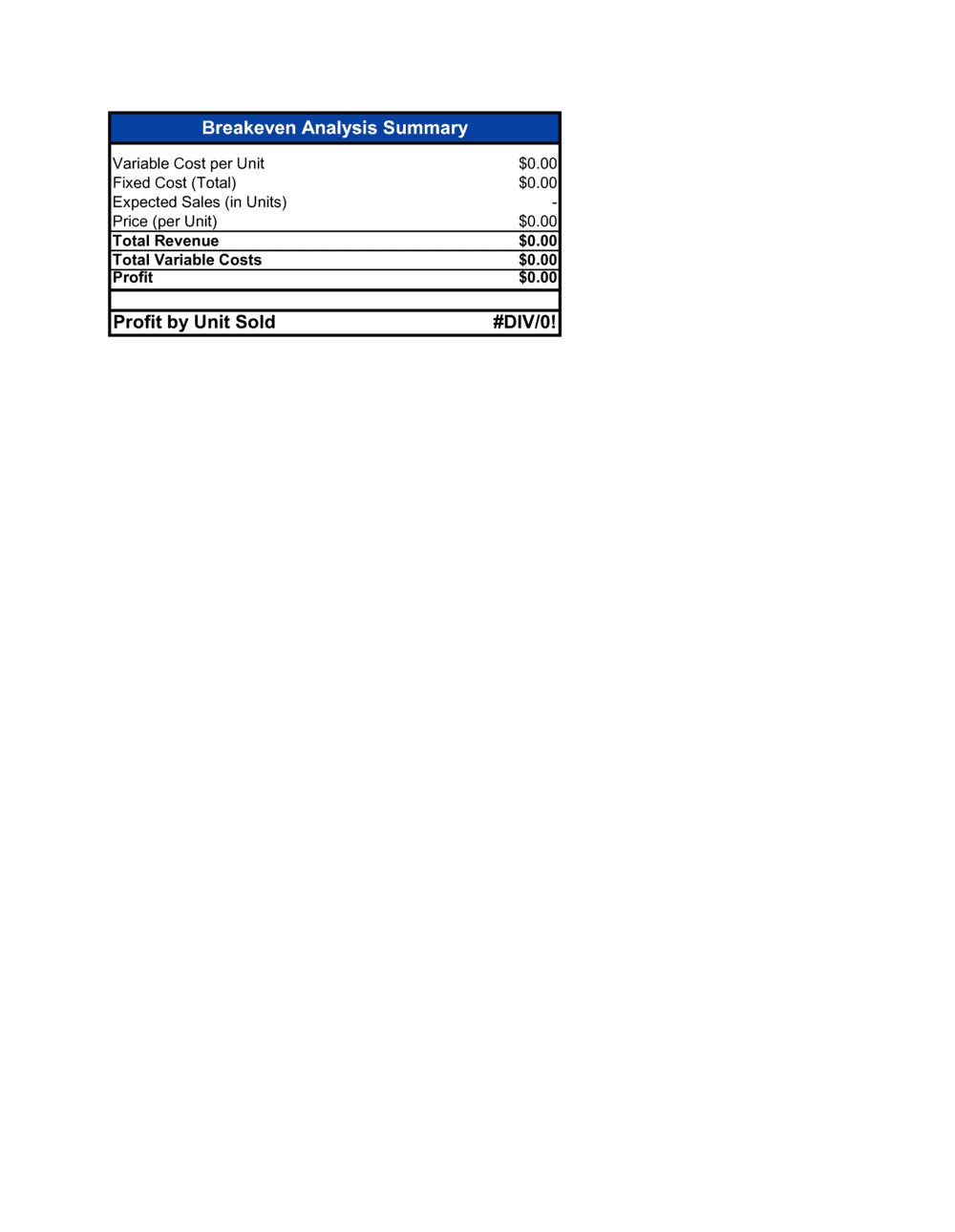

Enter each fixed cost as a separate line item — rent, utilities, salaries, loan repayments, insurance, software. Total them at the bottom of the schedule.

💡 Include owner or founder compensation as a fixed cost. If you exclude it, your BEP will be understated and the analysis will mislead any external reader.

3

Calculate variable cost per unit

List every cost that increases with each unit sold — materials, direct labor, packaging, shipping, commissions, and payment processing fees. Sum them to get your total variable cost per unit.

💡 Pull variable costs from recent supplier invoices and payroll records rather than estimates. Actual numbers produce a BEP you can rely on.

4

Enter the selling price per unit

Enter the price the customer pays, net of any standard discounts or rebates. Document the pricing basis (cost-plus, market, or value-based) so the analysis is self-explanatory to any reviewer.

💡 If you offer volume discounts, run a separate BEP for each pricing tier rather than averaging them.

5

Calculate contribution margin and contribution margin ratio

Subtract variable cost per unit from the selling price to get contribution margin per unit. Divide that figure by the selling price to get the contribution margin ratio.

💡 A contribution margin ratio below 30% typically signals a pricing or cost structure problem worth addressing before scaling.

6

Apply the BEP formulas

Divide total fixed costs by contribution margin per unit to get BEP in units. Divide total fixed costs by the contribution margin ratio to get BEP in revenue dollars. Enter both in the results section.

💡 Cross-check: BEP units multiplied by selling price should equal — or be very close to — your BEP in revenue dollars. A mismatch means a formula error.

7

Calculate the margin of safety

Subtract the BEP from projected or actual sales in both units and revenue. Divide by projected sales to get the margin of safety percentage.

💡 A margin of safety below 15% means a modest sales shortfall pushes the business into a loss. Flag this prominently when sharing the analysis with stakeholders.

8

Run and label the scenario analysis

Model at least three scenarios — base, optimistic, and pessimistic — by adjusting price, variable costs, or fixed costs. Label each scenario clearly and summarize the BEP range in a single conclusions paragraph.

💡 The gap between your optimistic and pessimistic BEP is more useful to a decision-maker than any single number — lead with the range in your summary.