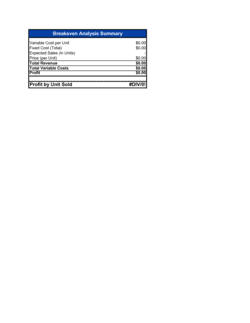

- Breakeven Point

- The sales volume — in units or revenue dollars — at which total revenues exactly equal total costs, producing zero profit or loss.

- Fixed Costs

- Costs that remain constant regardless of production or sales volume, such as rent, salaries, insurance, and depreciation.

- Variable Costs

- Costs that change in direct proportion to production or sales volume, such as raw materials, direct labor, and sales commissions.

- Contribution Margin

- Revenue minus variable costs — the amount each unit sold contributes toward covering fixed costs and generating profit.

- Contribution Margin Ratio

- Contribution margin expressed as a percentage of revenue, showing how many cents of each sales dollar cover fixed costs and profit.

- Margin of Safety

- The difference between actual or projected sales and the breakeven sales level — expressed in units or dollars — showing how far sales can fall before a loss occurs.

- Cost-Volume-Profit (CVP) Analysis

- A framework examining the relationship between costs, sales volume, and profit to support pricing, production, and strategic decisions.

- Target Profit Volume

- The sales volume required to achieve a specific profit goal, calculated by adding the target profit to fixed costs and dividing by the contribution margin per unit.

- Semi-Variable Cost

- A cost that has both a fixed base component and a variable component that changes with activity level, such as a utility bill with a fixed connection fee plus usage charges.

- Operating Leverage

- The degree to which a business relies on fixed costs; high operating leverage means profits grow rapidly above the breakeven point but losses deepen quickly below it.