Bookkeeping and Accounting Templates

★★★★★4.7from 280+ reviews· Trusted by 20M+ businesses

Track income, expenses, and records with ready-to-use templates built for every accounting task.

WordEditable onlinePDF21+ bookkeeping and accounting templates

Other Finance & Accounting categories

Most popular accounting templates

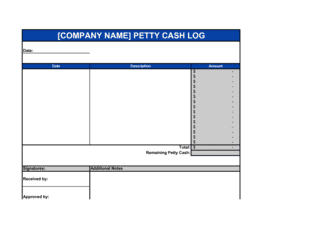

Day-to-day bookkeeping records

Expense tracking and budgeting

Compliance, policies, and record-keeping

Account management and correspondence

Hiring, guides, and planning

250K+Clients

20M+Free users

20+Years

190+Countries

10,000+Law firms

50M+Downloads

Trusted across review platforms

- Capterra★★★★☆4.649 reviews

- G2★★★★☆4.713 reviews

- GetApp★★★★☆4.649 reviews

- Google Play★★★★☆4.6179 ratings

- Google Reviews★★★★☆4.567 reviews

Frequently asked questions

What bookkeeping records does a small business need to keep?

At minimum, a small business needs a general ledger, accounts receivable and payable records, bank reconciliations, and expense statements. Most tax authorities also require payroll records, asset registers, and receipts for deductible expenses. The Checklist Key Record Keeping template in this folder provides a practical starting list. Retention requirements vary by jurisdiction, but seven years is a commonly cited benchmark for tax-related records.

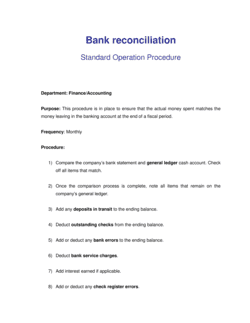

How often should I reconcile my bank accounts?

Monthly reconciliation is standard for most businesses and aligns with the bank statement cycle. Higher-volume businesses — retailers, restaurants, or any company processing many transactions daily — benefit from weekly reconciliation. Reconciling promptly after period close reduces the time needed to track down discrepancies and makes financial statements more reliable.

What is the difference between a general ledger and a subsidiary ledger?

A general ledger is the master record of all financial transactions organized by account type. Subsidiary ledgers (accounts receivable, accounts payable, inventory) record the detail behind a single general ledger account. For example, the accounts receivable subsidiary ledger lists every customer invoice; the general ledger shows only the total receivables balance. Both types of templates are included in this folder.

Do I need accounting software if I use these templates?

Not necessarily. For a very small business or sole proprietor with limited transactions, well-maintained spreadsheet templates can be sufficient. As transaction volume grows, accounting software reduces manual entry and the risk of formula errors. Many businesses use both: software for day-to-day entry and templates for specific analyses, policies, or audit-ready summaries.

How long should I retain financial records?

Retention requirements depend on the type of record and jurisdiction. In the US, the IRS generally recommends keeping tax records for at least three to seven years. Employment tax records typically must be kept for at least four years. Corporate records and asset registers may need to be kept indefinitely. The Financial Record Storage Guidelines template in this folder provides a structured framework for setting your own retention policy.

What goes in an accounting policies and procedures document?

An accounting policies and procedures document describes the methods your business uses to record and report financial activity: the accounting basis (cash or accrual), revenue recognition rules, depreciation methods, expense approval thresholds, and period-close procedures. It ensures consistency across staff, supports audits, and helps onboard new accounting employees.

Can I use these templates to prepare for a business audit?

Yes. Having organized, current ledgers, reconciliations, and policy documents significantly reduces the time and cost of an audit. Start by completing an Audit Information Legal Query to understand what records the auditor will request, then verify that your general ledger, bank reconciliations, and expense records are complete and cross-referenced.

What is a depreciation worksheet used for?

A depreciation worksheet calculates how much of a fixed asset's value is expensed each accounting period. It records the asset's original cost, the depreciation method applied (straight-line, declining balance, etc.), the useful life estimate, and the accumulated depreciation to date. Accurate depreciation tracking affects both net income on the income statement and the book value of assets on the balance sheet.

Bookkeeping and Accounting vs. related documents

Bookkeeping is the systematic recording of individual financial transactions — journal entries, ledger updates, reconciliations. Accounting is the broader discipline that interprets those records to produce financial statements, tax filings, and strategic analysis. Both functions rely on the same underlying documents, which is why templates in this folder serve both roles.

Accounting software (QuickBooks, Xero, FreshBooks) automates transaction entry and generates reports automatically. Accounting templates are simpler: editable spreadsheets or Word documents you fill in manually or semi-manually. Templates suit small businesses, project-specific needs, or teams that need a portable, shareable record outside their software system.

An operating budget projects revenues and expenses over a period to set spending targets. A cash flow forecast projects the timing of actual cash inflows and outflows to flag shortfalls before they happen. Most businesses need both; the operating budget guides decisions while the cash flow forecast manages liquidity. The Operating Budget template in this folder covers the first function.

Accounts receivable tracks money customers owe your business; accounts payable tracks money your business owes suppliers and vendors. Keeping both up to date is essential for accurate cash-flow visibility. This folder includes dedicated templates for each function.

Key clauses every Bookkeeping and Accounting contains

Most bookkeeping and accounting documents share a common set of fields and sections — understanding what each one does helps you complete them correctly.

- Party or account identification. Names the business, department, vendor, or customer the record relates to, preventing mix-ups across multiple accounts.

- Date range. Specifies the accounting period (daily, weekly, monthly, quarterly, or annual) the document covers.

- Opening balance. Records the starting figure carried forward from the previous period so running totals remain continuous.

- Transaction detail rows. Captures individual entries — date, description, amount, and category — that make the record auditable.

- Debit and credit columns. Separates outflows from inflows so each entry can be verified against the double-entry bookkeeping principle.

- Closing balance. Calculates the net position at the end of the period, ready to become the opening balance for the next one.

- Reconciliation or variance field. Compares the internal record to an external source (bank statement, invoice) and flags any difference.

- Authorized signature or approval line. Identifies who reviewed and approved the document, establishing accountability and supporting audit trails.

How to set up bookkeeping records for your business

Good bookkeeping starts with the right structure, not just the right numbers. Follow these steps to build a system that holds up at tax time and beyond.

1

Define your chart of accounts

List every account type your business uses — assets, liabilities, equity, revenue, and expenses — before recording a single transaction.

2

Choose your accounting period

Decide whether you'll close books monthly, quarterly, or annually, and apply that period consistently across all templates.

3

Record transactions in the general ledger

Enter every financial transaction with a date, description, debit, and credit so the ledger is always current.

4

Maintain subsidiary ledgers

Keep separate accounts receivable, accounts payable, and inventory records that feed into the general ledger.

5

Reconcile accounts regularly

Compare your ledger balances to bank statements and supplier invoices at least monthly to catch errors early.

6

Track and categorize expenses

Use expense statements and a business-deductions checklist to ensure every eligible cost is captured and correctly classified.

7

Document your policies and procedures

Record the accounting methods and rules your team follows so that records stay consistent when staff changes occur.

8

Store and back up financial records

Follow a retention schedule and backup policy so you can produce any record quickly during an audit or legal query.

At a glance

- What it is

- Bookkeeping and accounting templates are pre-structured documents that help businesses record financial transactions, track expenses, reconcile accounts, and maintain audit-ready records. They standardize how financial data is captured so that reporting is consistent and errors are easier to find.

- When you need one

- Any time you're recording transactions, preparing for tax season, reconciling bank statements, or organizing financial records, a ready-made template saves time and reduces the risk of mistakes.

Which Bookkeeping and Accounting do I need?

The right template depends on which bookkeeping or accounting task you're completing. Match your situation below to find the correct starting point.

Your situation

Recommended template

Recording all financial transactions for the business in one place

Centralizes every debit and credit entry for accurate period-end reporting.Matching your internal records to your monthly bank statement

Identifies discrepancies between your books and the bank's records.Tracking what customers owe and when payments are due

Monitors outstanding invoices so nothing slips through unpaid.Documenting employee or business travel and reimbursable costs

Captures itemized expenses with dates and categories for clean reimbursement.Calculating annual depreciation on equipment or property

Applies standard depreciation methods to fixed assets in a structured format.Setting up consistent accounting policies across the organization

Documents the rules and methods your team follows for every accounting task.Tracking quantities and values of stock on hand

Records stock movements so purchases, sales, and balances stay accurate.Planning the company's income and expenses for an operating period

Projects revenues and costs so spending stays aligned with financial goals.Glossary

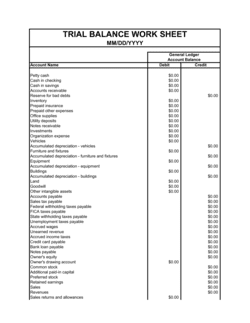

- General ledger

- The master accounting record that summarizes every financial transaction of a business, organized by account.

- Double-entry bookkeeping

- A system in which every transaction is recorded as both a debit in one account and a credit in another, keeping the books in balance.

- Bank reconciliation

- The process of matching a company's internal cash records against its bank statement to identify discrepancies.

- Accounts receivable

- Money owed to the business by customers for goods or services already delivered but not yet paid for.

- Accounts payable

- Money the business owes to suppliers or vendors for goods or services received but not yet paid for.

- Depreciation

- The systematic allocation of a fixed asset's cost over its useful life, reflecting the asset's gradual consumption of value.

- Chart of accounts

- An organized list of all account categories used by a business to record financial transactions.

- Operating budget

- A financial plan that projects expected revenues and expenses over a defined period to guide spending decisions.

- Accrual accounting

- An accounting method that records revenues and expenses when they are earned or incurred, regardless of when cash changes hands.

- Cash-basis accounting

- An accounting method that records revenues and expenses only when cash is actually received or paid.

- Audit trail

- A chronological record of all changes to financial data, enabling reviewers to trace any figure back to its original source document.

- Period close

- The process of finalizing all accounting entries for a defined period so that financial statements can be produced accurately.

What is a bookkeeping and accounting template?

A bookkeeping and accounting template is a pre-formatted document — spreadsheet, form, or structured Word file — that a business uses to record, organize, and report financial data. Rather than building a general ledger or bank reconciliation from scratch, you open a template with the correct columns, labels, and formulas already in place, enter your figures, and produce a clean, consistent record. Templates cover every layer of the accounting cycle: transaction recording, account reconciliation, expense tracking, asset depreciation, inventory valuation, and period-end reporting.

Bookkeeping templates focus on capturing raw financial data accurately and consistently. Accounting templates extend that data into analysis and decision support — budgets, depreciation schedules, policy documents, and audit-preparation tools. In practice, the same business uses both, often from the same folder, which is why this collection combines them.

When you need a bookkeeping or accounting template

The need arises any time financial data must be captured in a structured, retrievable format — whether that's a routine month-end close or a one-off task like responding to a bank request or disputing a charge. Good templates enforce consistency from the first entry, which makes audits, tax filings, and financial reviews much faster.

Common triggers:

- Closing the books at the end of a month, quarter, or year

- Reconciling your bank statement against internal records

- Tracking outstanding customer invoices and overdue balances

- Documenting employee expenses for reimbursement or tax purposes

- Calculating depreciation on vehicles, equipment, or property

- Onboarding a new bookkeeper or accounting technician who needs standardized forms

- Preparing records ahead of an external audit or tax review

- Building an operating budget for the next financial period

- Establishing written accounting policies to ensure consistency across staff

Without structured records, small discrepancies compound over time into material errors that are expensive to unwind. A set of well-maintained bookkeeping templates provides the paper trail that protects the business — whether the question comes from a tax authority, an investor, or an internal review.

Award-winning platform

- Great Place to Work 2025

- BIG Award — Product of the Year 2025

- Smartest Companies 2025

- Global 100 Excellence 2026

- Best of the Best 2025