1

Identify both parties and their roles

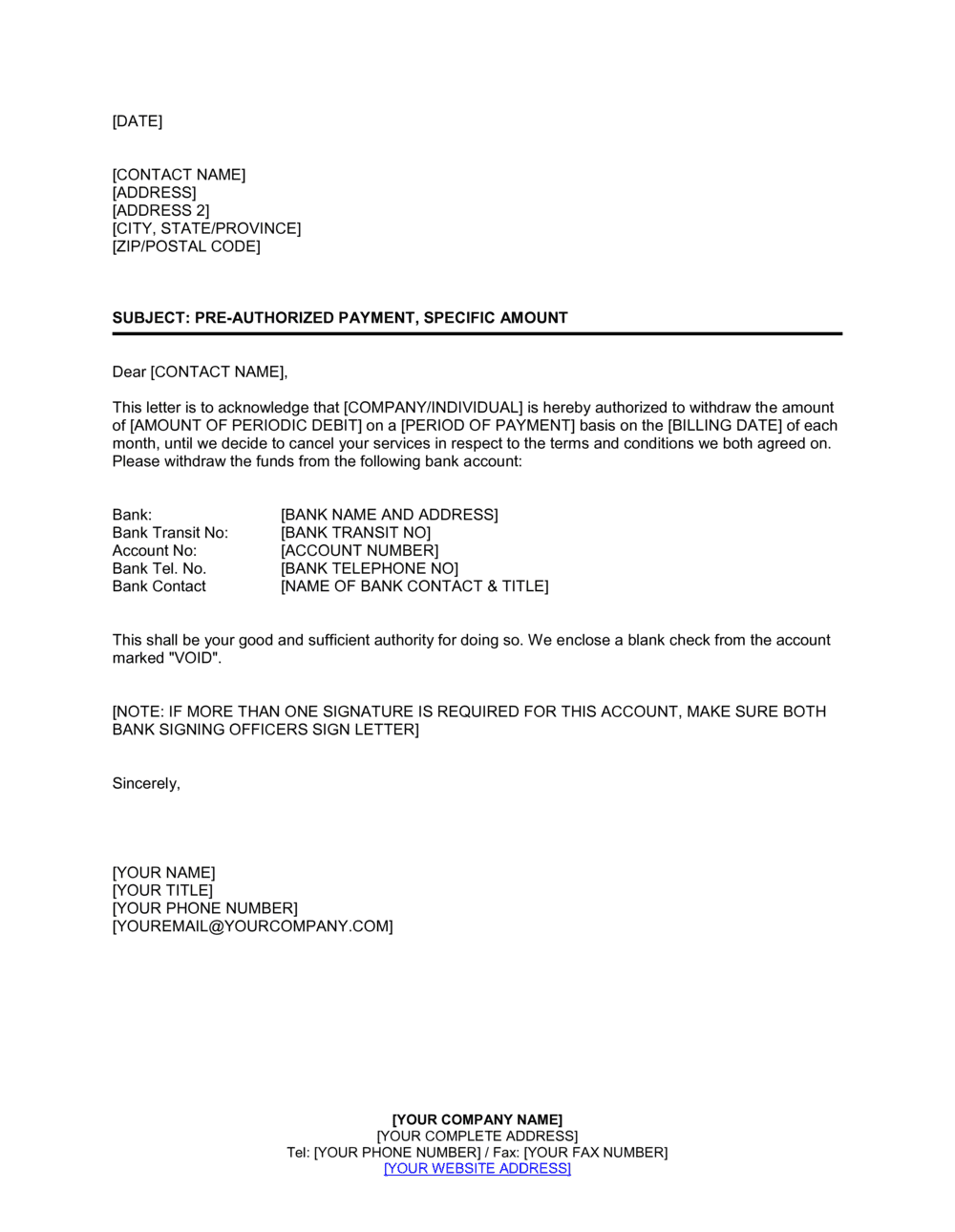

Enter the payee's full legal business name and contact details, and the payer's full legal name and current address. Confirm that the payer is the actual account holder — not a third party — before proceeding.

💡 If the payer is a business rather than an individual, identify the authorized signatory by name and title to ensure the authorization is binding on the entity.

2

Record the complete bank account details

Enter the payer's bank name, full account number, and routing or transit number exactly as they appear on a voided cheque or bank statement. Attach a voided cheque to the signed form as standard practice.

💡 Ask the payer to attach a voided cheque to the signed authorization — it confirms all banking details match and significantly reduces failed-debit rates.

3

State the fixed debit amount precisely

Enter the exact dollar and cent amount to be debited each cycle — written numerically and in words. Do not use ranges or 'up to' language; this must be a single fixed figure.

💡 If the amount will ever change (e.g., annual price increases), use a variable-amount PAD form instead, or include an amendment clause requiring fresh written consent before the new amount takes effect.

4

Set the frequency, start date, and number of payments

Specify the billing cycle (weekly, monthly, quarterly, or annually), the calendar date of the first debit, and either the total number of payments authorized or the condition that terminates the authorization.

💡 Tie the authorization's end date to the underlying contract term — this prevents debits from continuing after the service or membership agreement lapses.

5

Describe the purpose of the payments

Write a specific, plain-English description of what the recurring payment covers — for example, 'monthly gym membership fees under the Membership Agreement dated [DATE].' Reference the underlying agreement by name and date.

💡 A specific purpose clause reduces successful chargeback claims: it gives the payer's bank clear evidence that the debit was tied to a known commercial obligation.

6

Include the cancellation and dispute provisions

Confirm the cancellation notice period (typically 10–30 days before the next debit), the delivery method for cancellation notices, and the dispute window and contact details for the reimbursement procedure.

💡 Match your cancellation notice requirement to the applicable banking scheme minimum — do not exceed 30 days for consumer payers, as most banking rules cap it there.

7

Execute before the first debit date

Both parties should sign and date the authorization before the first scheduled debit is processed. Provide the payer with a copy of the signed authorization at the time of execution.

💡 Retain a copy of the signed authorization — including the attached voided cheque — for the entire duration of the agreement plus at least 2 years after the last debit, to defend against reimbursement claims.

8

Submit to your payment processor and file the original

Provide the completed authorization to your bank, payment processor, or ACH originator as required by their onboarding process. File the executed original in a secure, retrievable system.

💡 Some processors require a digital copy of the signed authorization before activating the debit series — confirm your processor's specific submission requirements before the first billing date.