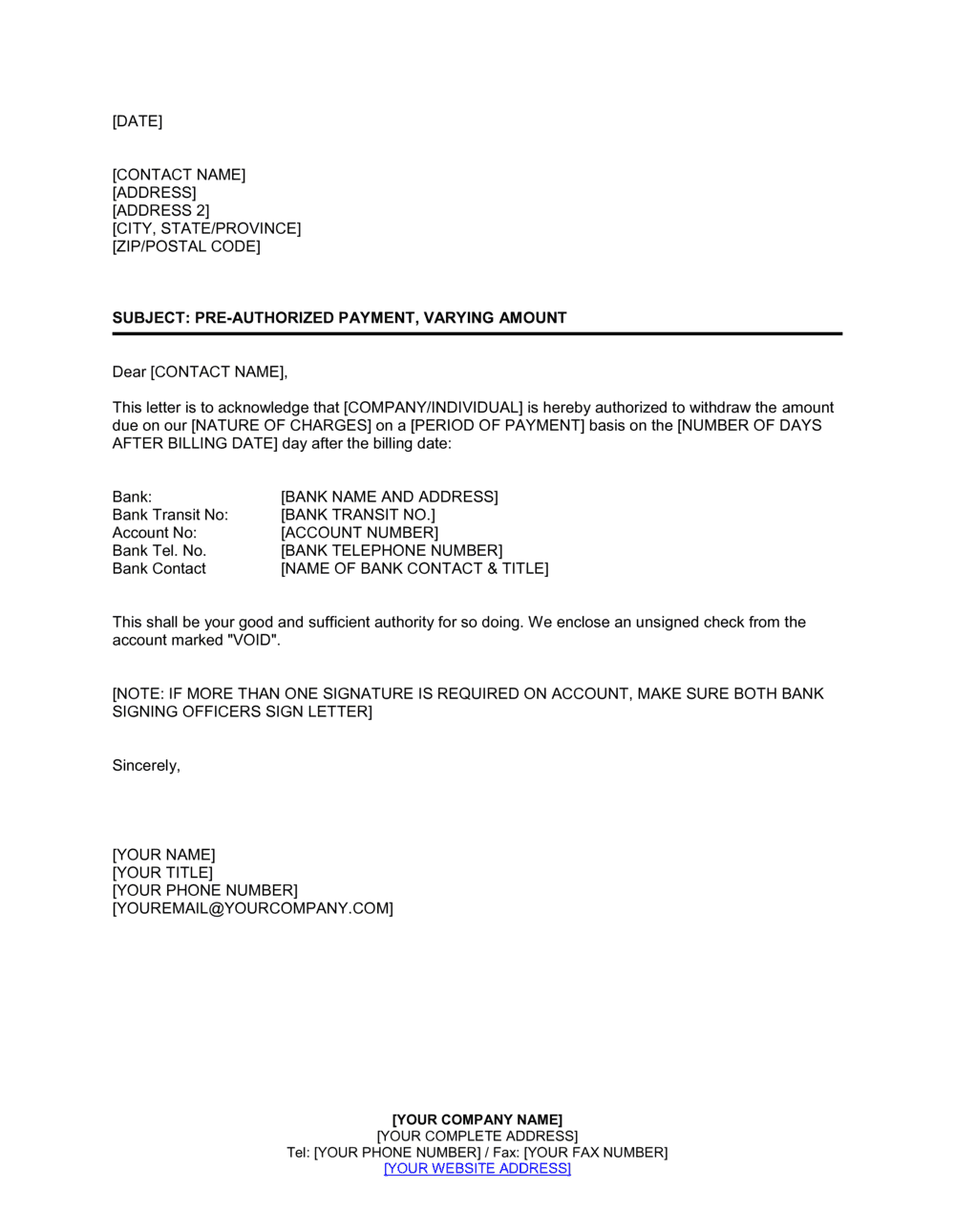

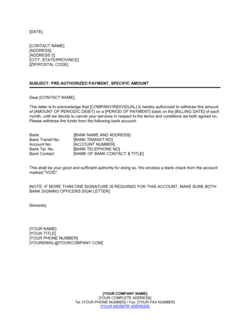

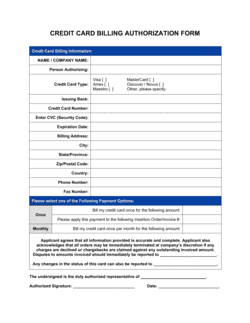

1

Identify both parties and their roles

Enter the payor's full legal name (individual or business entity) and the payee's registered business name. For business payors, include the authorized signatory's name and title.

💡 For consumer authorizations, use the name exactly as it appears on the bank account to avoid processing mismatches.

2

Record the full bank account details

Enter the financial institution name, the full routing or transit number, and the complete account number. Do not use masked or partial account numbers on the authorization form itself — keep the signed original in a secure, access-controlled location.

💡 Scan and store the signed original in an encrypted document vault; never transmit the signed form by unencrypted email.

3

Specify the exact payment amount and frequency

State the dollar amount to the cent for fixed payments. For variable amounts, describe the formula or cap clearly — for example, 'the monthly invoice total, not to exceed $[MAXIMUM AMOUNT].' Set the recurrence interval and the specific day of the week or month the debit will run.

💡 If your business uses tiered pricing that changes at contract renewal, add a notice-of-change period of at least 10 business days to avoid compliance failures.

4

Set the start date and termination condition

Enter the first debit date and choose a termination condition: a specific end date, a total number of payments, a balance reaching zero, or an open-ended authorization that runs until revoked. Match the termination condition to the underlying agreement's payment schedule.

💡 For installment loans, calculate the exact number of payments and state it explicitly — 'this authorization covers [24] monthly debits' — rather than relying on an open-ended authorization.

5

Set the NSF fee and retry policy

Enter your NSF fee amount (verify the statutory cap in the payor's jurisdiction) and state the maximum number of retry attempts and the window within which retries will occur. Two retries within 10 business days is the standard commercial practice.

💡 Inform your payment processor of your retry policy — some processors have their own network rules that override the number of retries in your authorization form.

6

Include the dispute rights and cancellation procedure

State the payor's right to dispute an unauthorized debit and the 90-day window for filing with their bank. Describe the cancellation procedure — written notice, minimum advance notice period, and the exact address or email for revocation notices.

💡 For Canadian PADs, the dispute window is 90 days for unauthorized debits and 10 business days for debits that do not comply with the authorization — include both in your form.

7

Cross-reference the underlying agreement

Enter the name, date, and parties of the contract, lease, or loan agreement that creates the underlying payment obligation. This prevents the payor from arguing that revoking the authorization eliminates the debt itself.

💡 Attach a copy of the underlying agreement to the PAD authorization at signing so both documents share the same execution date.

8

Obtain a wet or electronic signature before the first debit

Both parties should sign and date the form before the first scheduled debit runs. For electronic signatures, use a compliant e-signature platform that captures a timestamp and IP address.

💡 Send the signed copy to the payor immediately after execution — Payments Canada Rule H1 requires that the payor receive a copy of their signed authorization.