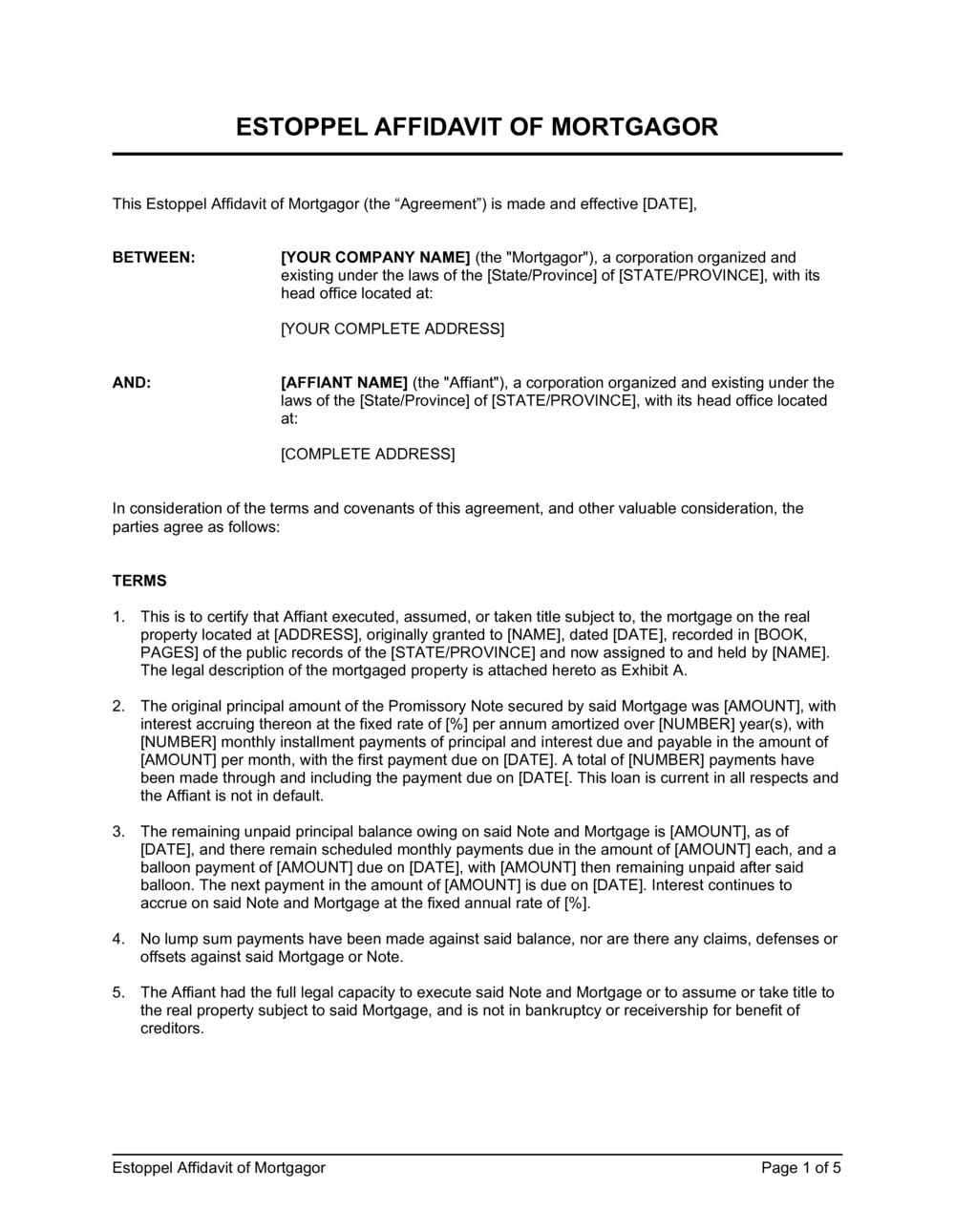

1

Gather the original loan documents

Collect the original mortgage note, deed of trust, and any recorded modifications or forbearance agreements before completing any field. Every certified figure must match the lender's payment history and recorded instruments.

💡 Request a formal payoff or loan status letter from your lender dated within 10 days of the affidavit — this is the authoritative source for the principal balance and payment status.

2

Enter the full legal names of all parties

Use the mortgagor's exact legal name as it appears on the original loan documents and the deed. Use the mortgagee's full registered entity name. Abbreviations or trade names that differ from recorded instruments can create title defects.

💡 If the mortgagee has changed its name or been acquired since the loan was originated, use the current legal name and reference the predecessor in a parenthetical.

3

Insert the property legal description

Copy the legal description from the recorded deed or title commitment exactly — lot number, block, subdivision, and county. Do not substitute a street address for the legal description in this field.

💡 Pull the legal description directly from the county recorder's digital record to eliminate transcription errors that could invalidate the affidavit.

4

Certify the outstanding principal balance and rate

Enter the exact principal balance as of the certification date, the interest rate (and whether fixed or adjustable), and the monthly payment amount. For adjustable-rate loans, state the current rate and the next adjustment date.

💡 Use a certification date that is as close as possible to the closing date — lenders typically accept certifications within 30 days, but title companies may require 10 days or fewer.

5

Confirm payment status and last payment date

State the date the last payment was received and the period it covered. Explicitly state whether the loan is current or in default. If in default, describe the nature and amount of the delinquency.

💡 Do not estimate the last payment date from memory — retrieve the confirmation number or bank statement showing the payment was received, not just sent.

6

Disclose all modifications and side agreements

List every loan modification, deferral, forbearance agreement, or rate adjustment by date. If none exist, write 'None' explicitly — leaving the field blank is not equivalent and may be treated as incomplete.

💡 Include COVID-era forbearance agreements even if the deferred amounts have been repaid — note buyers conduct due diligence on the loan history and undisclosed forbearance is a common red flag.

7

Review and sign before a notary public

Read every certified statement against your source documents before appearing before the notary. Sign only in the notary's presence, with valid government-issued photo identification available for verification.

💡 Schedule the notarization within 5 business days of the closing date to ensure the certification date aligns with the lender's expectation for a current statement.

8

Deliver the executed original to the requesting party

Provide the wet-signed, notarized original to the title company, buyer's counsel, or lender as specified in the closing instructions. Retain a certified copy for your records.

💡 Confirm whether the recipient requires the original or will accept a notarized copy — some title insurers require the original for their policy file.