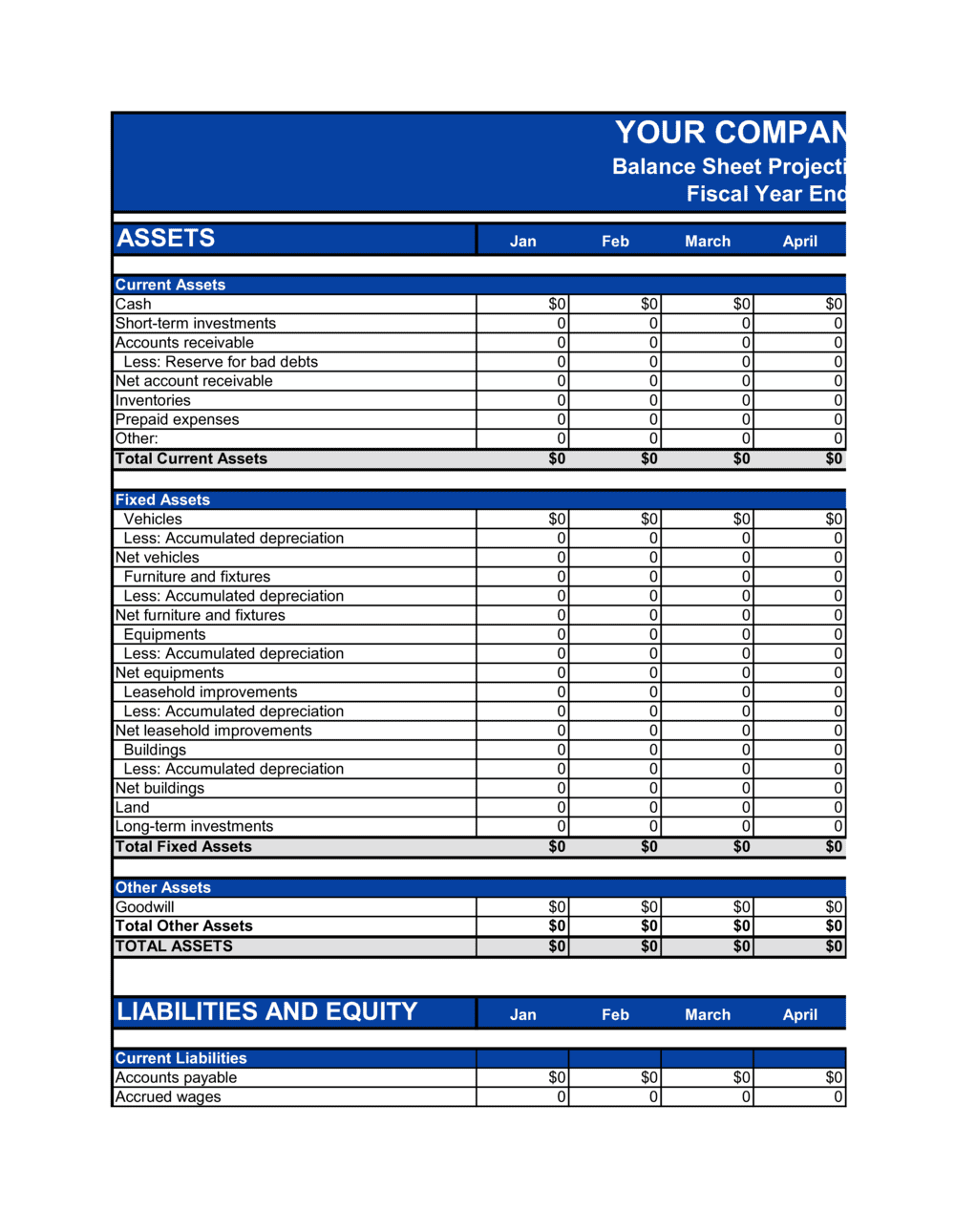

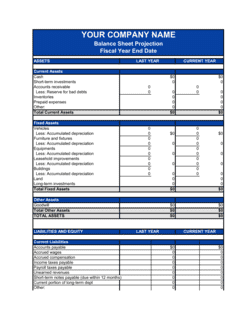

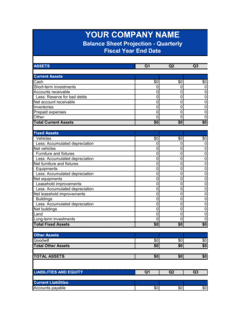

- Accounting Equation

- The foundational rule that Total Assets must equal Total Liabilities plus Total Equity — if the balance sheet does not balance, an entry error exists.

- Current Assets

- Assets expected to be converted to cash or consumed within 12 months, including cash, accounts receivable, and inventory.

- Non-Current Assets

- Assets held for longer than 12 months, such as property, equipment, and intangible assets like patents or goodwill.

- Current Liabilities

- Obligations due within 12 months, including accounts payable, accrued expenses, and the current portion of long-term debt.

- Long-Term Liabilities

- Obligations not due within the next 12 months, such as term loans, bonds payable, and deferred tax liabilities.

- Shareholders' Equity

- The residual interest in the company's assets after all liabilities are deducted — consisting of paid-in capital, retained earnings, and any accumulated other comprehensive income.

- Retained Earnings

- Cumulative net income earned since inception minus all dividends or distributions paid to shareholders to date.

- Working Capital

- Current Assets minus Current Liabilities — a measure of short-term liquidity indicating whether the business can meet its near-term obligations.

- Depreciation

- The systematic allocation of a tangible asset's cost over its useful life, reducing the asset's book value on the balance sheet each period.

- Goodwill

- An intangible asset recorded when one company acquires another for more than the fair value of its identifiable net assets.

- Accrued Liabilities

- Expenses incurred but not yet paid as of the statement date — such as unpaid wages, interest, or taxes — recorded to match costs to the correct period.

- Liquidity Ratio

- A metric derived from balance sheet figures — such as the current ratio or quick ratio — measuring the company's ability to pay short-term obligations.