- GAAS (Generally Accepted Auditing Standards)

- The set of standards issued by the AICPA in the US that govern how an auditor plans, performs, and reports on a financial-statement audit.

- ISA (International Standards on Auditing)

- Auditing standards issued by the IAASB, adopted in over 130 countries, that establish the principles and requirements for audit engagements outside the US.

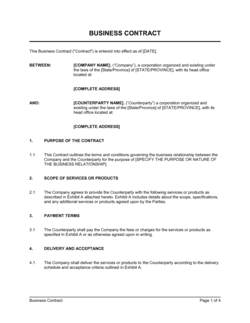

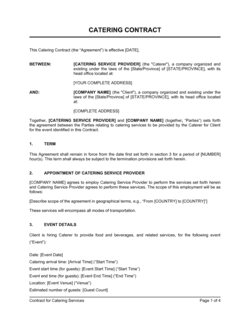

- Engagement Letter

- A written contract between an auditor and a client that confirms the terms of the audit engagement before work begins — functionally equivalent to an audit contract.

- Auditor Independence

- The requirement that an external auditor has no financial, personal, or business relationship with the client that could impair objective judgment or create the appearance of bias.

- Management Representation Letter

- A letter signed by management at the conclusion of the audit confirming the completeness and accuracy of information provided to the auditor.

- Materiality

- A threshold, typically expressed as a percentage of revenue or total assets, below which misstatements are judged unlikely to influence the decisions of financial statement users.

- Audit Opinion

- The formal conclusion issued by the auditor after completing fieldwork — unqualified, qualified, adverse, or disclaimer — on whether the financial statements present fairly in all material respects.

- Scope Limitation

- A restriction on the auditor's ability to obtain sufficient evidence — caused by client limitations or circumstances — that may result in a qualified or disclaimer opinion.

- Subsequent Events

- Events or transactions that occur after the balance-sheet date but before the audit report is issued, which may require disclosure or adjustment to the financial statements.

- Agreed-Upon Procedures

- A limited engagement where the auditor performs specific procedures agreed to by the client and any relevant third parties, without expressing an overall audit opinion.

- Going Concern

- An auditor's assessment of whether a company has the ability to continue operating for at least twelve months from the balance-sheet date.