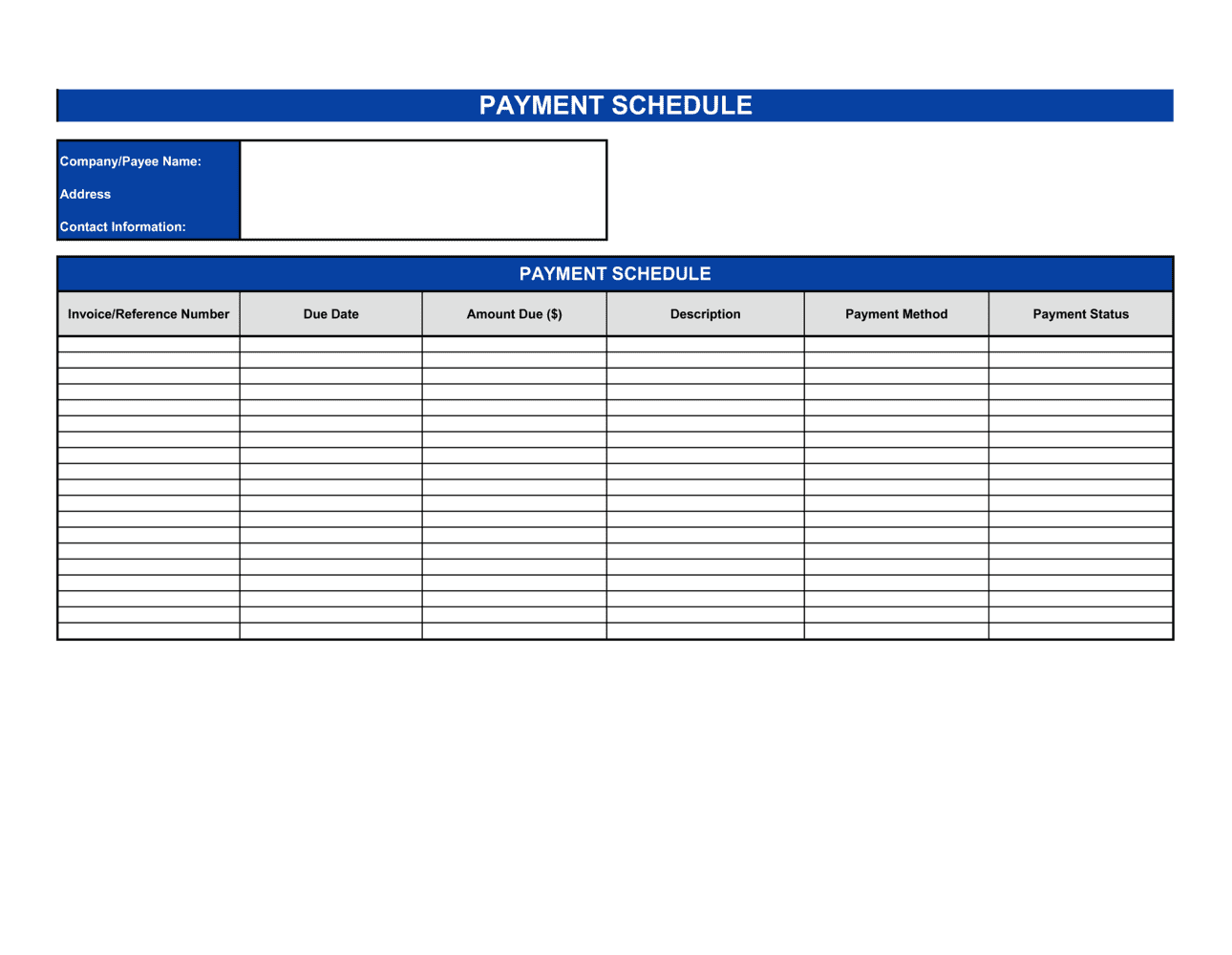

❌ Using relative due dates instead of specific calendar dates

Why it matters: Terms like 'due on the 1st of each month' create disputes when months start on weekends or holidays, and make it impossible to calculate the exact default date.

Fix: List every due date as a specific MM/DD/YYYY entry in the table so both parties have a single, unambiguous record.