- Commitment Letter

- A written statement from a lender or investor confirming their intent to provide financing under specific terms, typically issued before formal loan documents are executed.

- Conditions Precedent

- Requirements the borrower or investee must satisfy before the lender is obligated to fund — such as delivering financial statements, appraisals, or corporate approvals.

- Commitment Fee

- A fee charged by a lender to hold financing available for a borrower during the commitment period, typically expressed as a percentage of the committed amount.

- Expiration Date

- The deadline by which the borrower must accept the commitment and satisfy all conditions, after which the lender's obligation lapses.

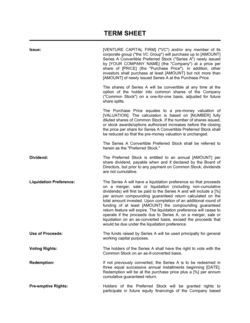

- Term Sheet

- A preliminary, often non-binding document summarizing the key economic and structural terms of a proposed financing or investment, which a commitment letter formalizes.

- Due Diligence

- The process by which a lender or investor investigates a borrower's financial condition, legal standing, and collateral before committing to fund.

- Binding vs. Non-Binding Letter

- A binding commitment letter creates enforceable obligations on both parties; a non-binding letter confirms intent only and may be withdrawn subject to final diligence or approval.

- Closing Conditions

- Specific actions or deliverables — such as executing loan documents, obtaining insurance, or clearing title — that must occur before funds are disbursed.

- Drawdown

- The act of a borrower requesting and receiving all or part of committed funds under an approved facility.

- Collateral

- An asset pledged by the borrower to secure repayment of a loan — if the borrower defaults, the lender may seize and sell the collateral to recover the debt.