1

Identify the parties and transaction type

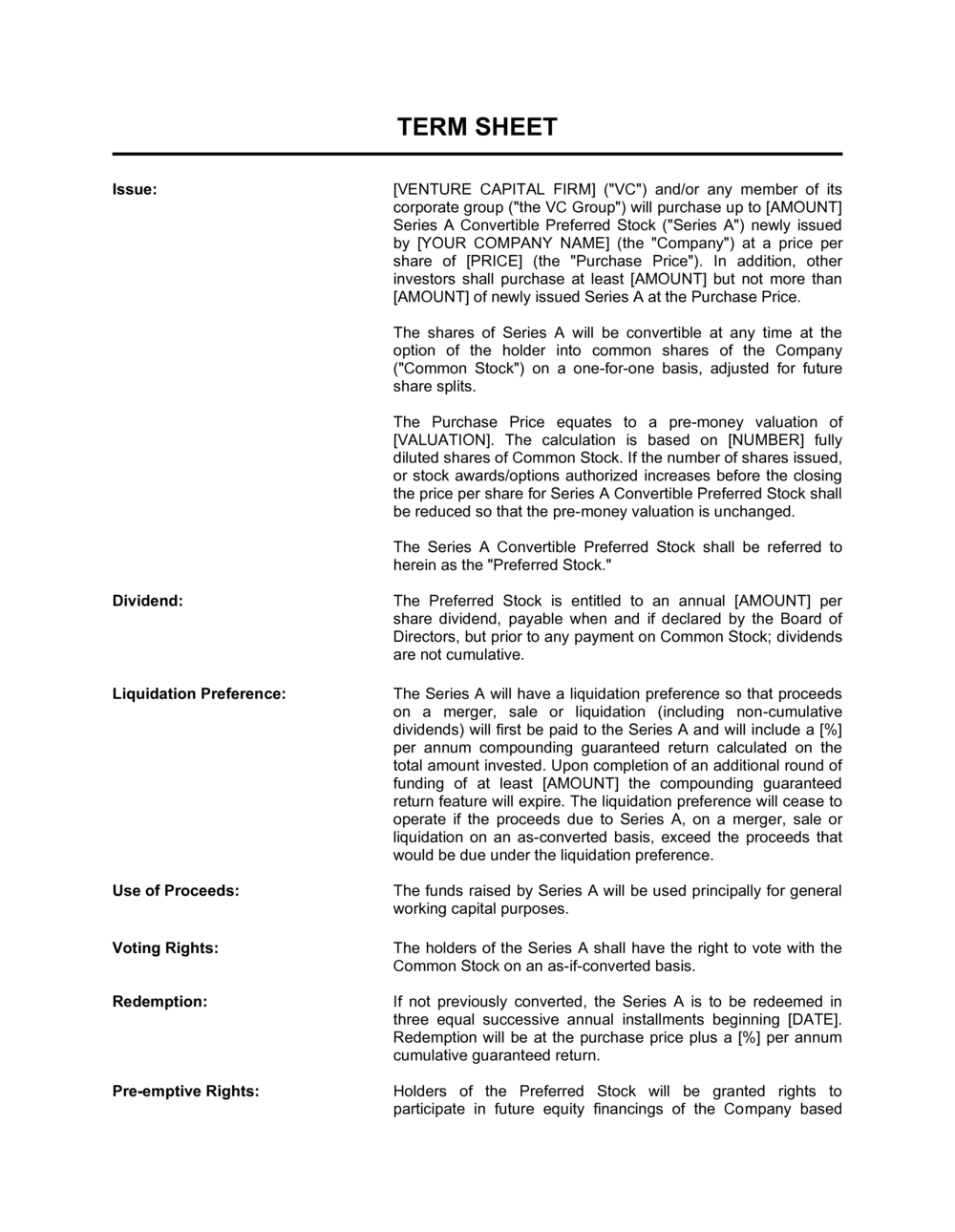

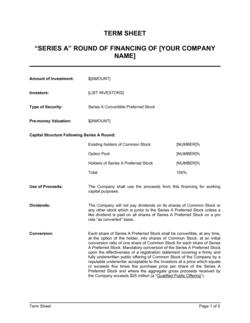

Enter the company's full registered legal name, the investor's or acquirer's legal entity name, and a one-line description of the transaction type — equity investment, debt financing, or acquisition. Do not use trade names or 'doing business as' names.

💡 Confirm the exact legal entity name against the company's certificate of incorporation or equivalent registry filing before the counterparty signs.

2

Set the valuation and investment amount

Agree on pre-money valuation, total round size, and resulting investor ownership. Specify explicitly whether the employee option pool is sized before or after the new money — this single assumption can shift founder dilution by several percentage points.

💡 Attach a pro forma cap table as Exhibit A showing fully-diluted ownership both before and after closing, including the post-closing option pool.

3

Define the security type and share structure

Specify the exact class of security — Series A Preferred, convertible note, SAFE, or common stock — and the price per share or conversion mechanics. Reference the post-closing cap table for context.

💡 For convertible notes and SAFEs, make sure the valuation cap and discount rate are both stated explicitly — ambiguity on either triggers disputes at the priced round.

4

Negotiate liquidation preference and participation

State the preference multiple (1× is market standard for most VC deals) and whether preferred is participating or non-participating. Non-participating preferred is standard for Series A; participating preferred is common in bridge rounds and some growth deals.

💡 If the investor insists on participating preferred, negotiate a hard cap — typically 2–3× the original investment — above which preferred converts to common and participates without the separate preference.

5

Fill in governance and protective provisions

Set board size and composition, list which actions require investor consent, and specify any voting thresholds. Tie dollar thresholds to each veto right — e.g., debt incurrence above $500K — rather than leaving them open-ended.

💡 Standard NVCA market terms cap the investor consent list at six to eight items. A list exceeding twelve protective provisions is a red flag that the investor is seeking operational control beyond their economic stake.

6

Specify binding versus non-binding provisions

Mark every clause as either 'binding' or 'non-binding (for discussion purposes only).' Only the exclusivity, confidentiality, governing law, and expense clauses should be binding. Every economic and governance term should be non-binding until definitive agreements are signed.

💡 Add a standalone paragraph at the top of the term sheet stating clearly that, except for the listed binding provisions, the term sheet does not constitute a legally binding obligation on either party.

7

Set the exclusivity period and conditions to closing

Enter a specific exclusivity end date — 30 to 60 days is market standard — and list the conditions to closing with enough specificity that neither party can invoke them arbitrarily.

💡 Tie the exclusivity period to a specific due diligence checklist delivery date. If the investor hasn't requested materials within 10 business days, the exclusivity clock should pause.

8

Cap legal fee reimbursement and sign before exclusivity begins

Insert a specific dollar cap on investor legal fee reimbursement (typically $15,000–$35,000 for a seed deal, $35,000–$75,000 for a Series A). Both parties should sign and date the term sheet before the exclusivity period starts running.

💡 Use a dated electronic signature to establish the exact moment exclusivity begins — this matters if the investor later argues the no-shop period expired before a competing offer arrived.