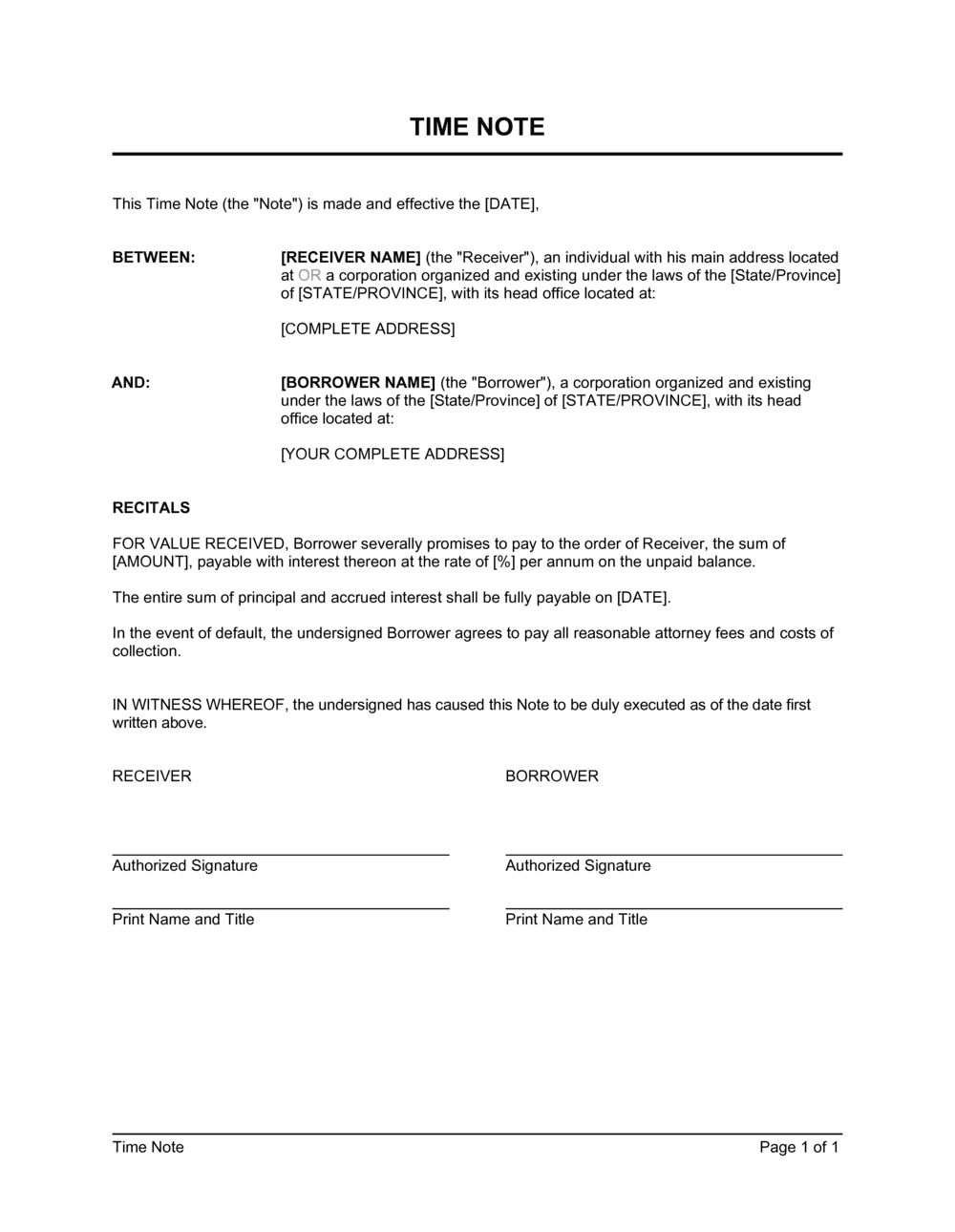

1

Identify both parties with full legal names

Enter the borrower's (Maker's) and lender's (Payee's) complete registered legal entity names, entity types, states of formation, and principal business addresses. For individuals, use the full legal name as it appears on government-issued ID.

💡 Pull the exact entity name from the relevant state's secretary of state business registry to ensure it matches official records.

2

Enter the principal amount in figures and words

State the loan amount numerically and spell it out in full words on the same line. Confirm the amount matches any accompanying loan agreement or board resolution authorizing the borrowing.

💡 For amounts above $100,000, consider having both parties initial next to the principal figure to deter any later claim of alteration.

3

Set the interest rate and confirm it is below the usury ceiling

Enter the annual interest rate and specify simple or compound accrual. Before finalizing, verify the rate does not exceed the usury limit for the governing jurisdiction — limits vary widely by state and loan type.

💡 For inter-company loans between related entities, the IRS requires a minimum interest rate (the Applicable Federal Rate) to avoid imputed income treatment — check the current AFR before setting the rate.

4

Define the payment schedule and maturity date

Specify whether the note is a pure bullet (lump sum at maturity), periodic interest with bullet principal, or a defined installment schedule. State the exact maturity date — day, month, and year — in unambiguous format.

💡 Use the format 'December 31, 2027' rather than '12/31/27' to avoid date-format ambiguity in cross-border transactions.

5

Set the cure period for payment default

In the events-of-default clause, enter the number of days the borrower has to cure a missed payment before the note is formally in default. Three to ten business days is typical for commercial notes.

💡 A longer cure period (five to ten days) reduces the risk that a wire-transfer delay or bank processing issue triggers an unintended default.

6

Confirm prepayment and application-of-payments terms

State whether the borrower may prepay without penalty and specify how any partial payments are applied — interest first, then principal — to avoid ambiguity in the borrower's payoff calculations.

💡 If the lender wants to earn a minimum return, add a prepayment premium formula (e.g., 2% of prepaid principal in the first 12 months) rather than leaving the clause silent.

7

Choose the governing law with a real connection to the transaction

Select the state or country where the lender is located, where the borrower operates, or where loan proceeds will be used. Confirm the chosen jurisdiction's usury laws permit the agreed interest rate.

💡 Avoid selecting a governing law solely because it has favorable usury limits if neither party has any operational presence there — courts may decline to honor the choice.

8

Execute before funds are disbursed

Both parties must sign the note before or simultaneously with the transfer of loan proceeds. Have each signatory date the document personally. Retain an original signed copy and provide a copy to the borrower.

💡 For higher-value notes, consider having signatures notarized — it is not legally required in most jurisdictions but significantly strengthens evidentiary weight if the note is later disputed in court.