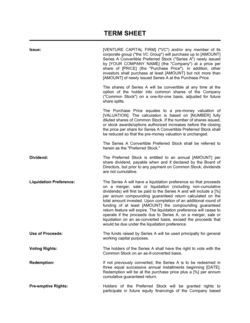

- Convertible Note

- A short-term debt instrument that converts into equity at a future financing round rather than being repaid in cash.

- Principal

- The original loan amount the investor provides to the company under the note.

- Valuation Cap

- The maximum company valuation at which the note will convert into equity, giving early investors a lower price per share than later investors in the same round.

- Discount Rate

- A percentage reduction on the price per share at conversion, rewarding the noteholder for investing earlier than equity investors — typically 10–25%.

- Qualified Financing

- A future equity financing that meets a minimum size threshold defined in the note, triggering automatic conversion of the outstanding principal and accrued interest.

- Maturity Date

- The date by which the note must convert, be repaid, or be renegotiated if a qualified financing has not occurred.

- Accrued Interest

- Interest that accumulates on the principal over time and is typically added to the conversion amount rather than paid in cash.

- Pre-Money Valuation

- The company's agreed value immediately before a new investment round, used as the basis for calculating price per share at conversion.

- Pro Rata Rights

- A noteholder's contractual right to invest in subsequent financing rounds in proportion to their existing ownership, preventing dilution.

- Change of Control

- A transaction in which ownership or control of the company shifts — typically a merger, acquisition, or asset sale — that may trigger early repayment or conversion.

- SAFE

- Simple Agreement for Future Equity — a non-debt alternative to a convertible note that also defers valuation, but carries no interest rate or maturity date.