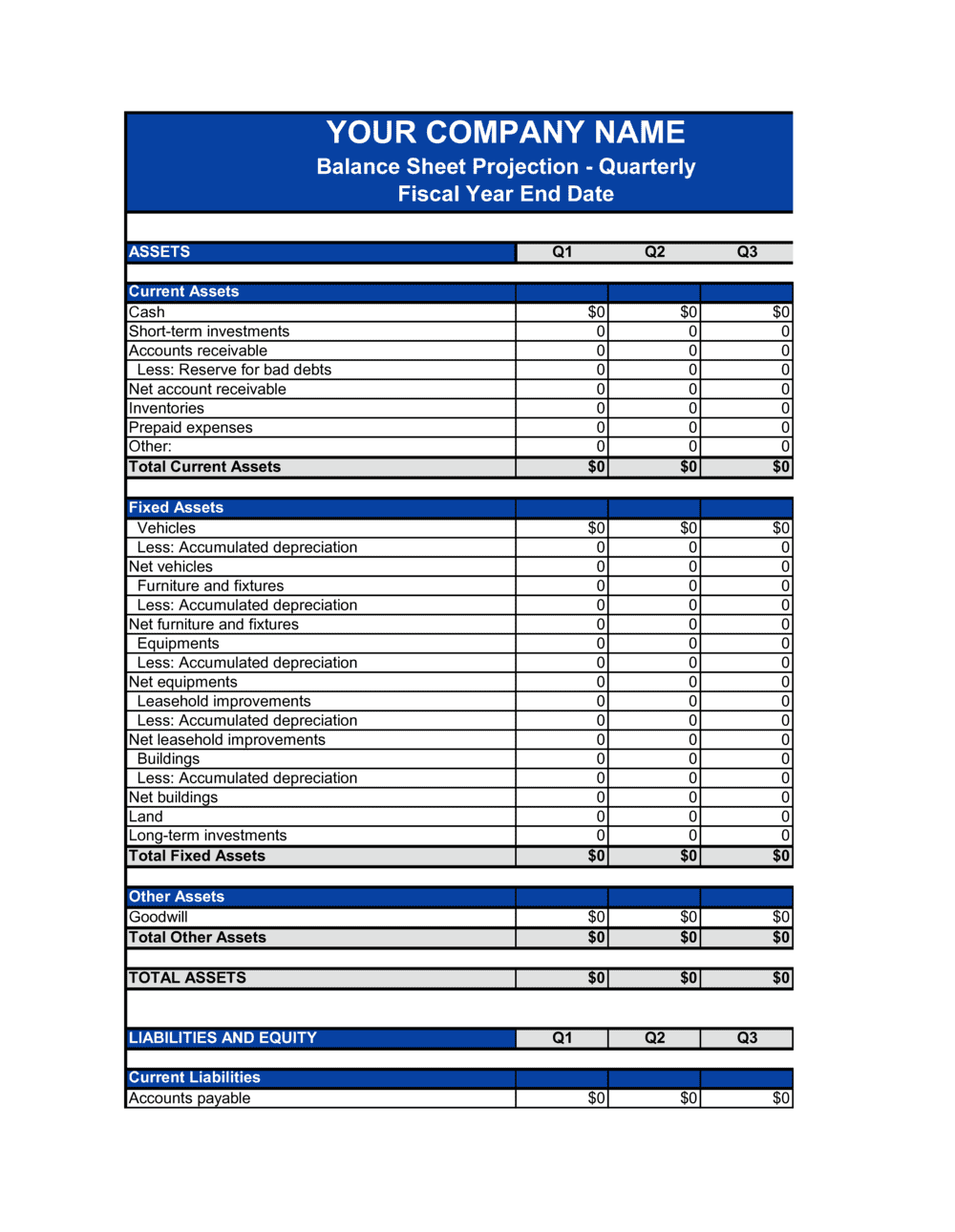

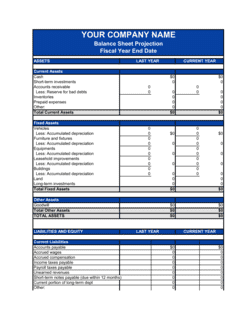

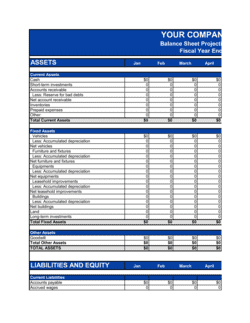

- Current Assets

- Assets expected to be converted to cash or used within 12 months, including cash, accounts receivable, inventory, and prepaid expenses.

- Non-Current Assets

- Long-term assets not expected to be liquidated within 12 months, such as property, plant, equipment, and intangible assets.

- Current Liabilities

- Obligations due within 12 months, including accounts payable, accrued expenses, short-term debt, and the current portion of long-term debt.

- Non-Current Liabilities

- Debt and obligations maturing beyond 12 months, such as long-term bank loans, bonds payable, and deferred tax liabilities.

- Shareholders' Equity

- The residual interest in assets after all liabilities are deducted — comprising paid-in capital, retained earnings, and accumulated other comprehensive income.

- Retained Earnings

- Cumulative net income earned since inception minus all dividends or distributions paid to owners.

- Working Capital

- Current assets minus current liabilities — the net short-term liquidity available to fund day-to-day operations.

- Accounting Period

- The specific date as of which the balance sheet is prepared — for a quarterly statement, typically the last calendar day of the fiscal quarter.

- Comparative Period

- The prior-period balance sheet column shown alongside the current period to allow readers to identify trends and changes in financial position.

- Going Concern

- The assumption that a business will continue operating for the foreseeable future — a going-concern qualification from an auditor signals material doubt about this assumption.

- Accrual Basis

- An accounting method that records revenues when earned and expenses when incurred, regardless of when cash changes hands — the basis required for GAAP-compliant balance sheets.

- Intangible Assets

- Non-physical assets with economic value, such as patents, trademarks, software licenses, and goodwill arising from a business acquisition.