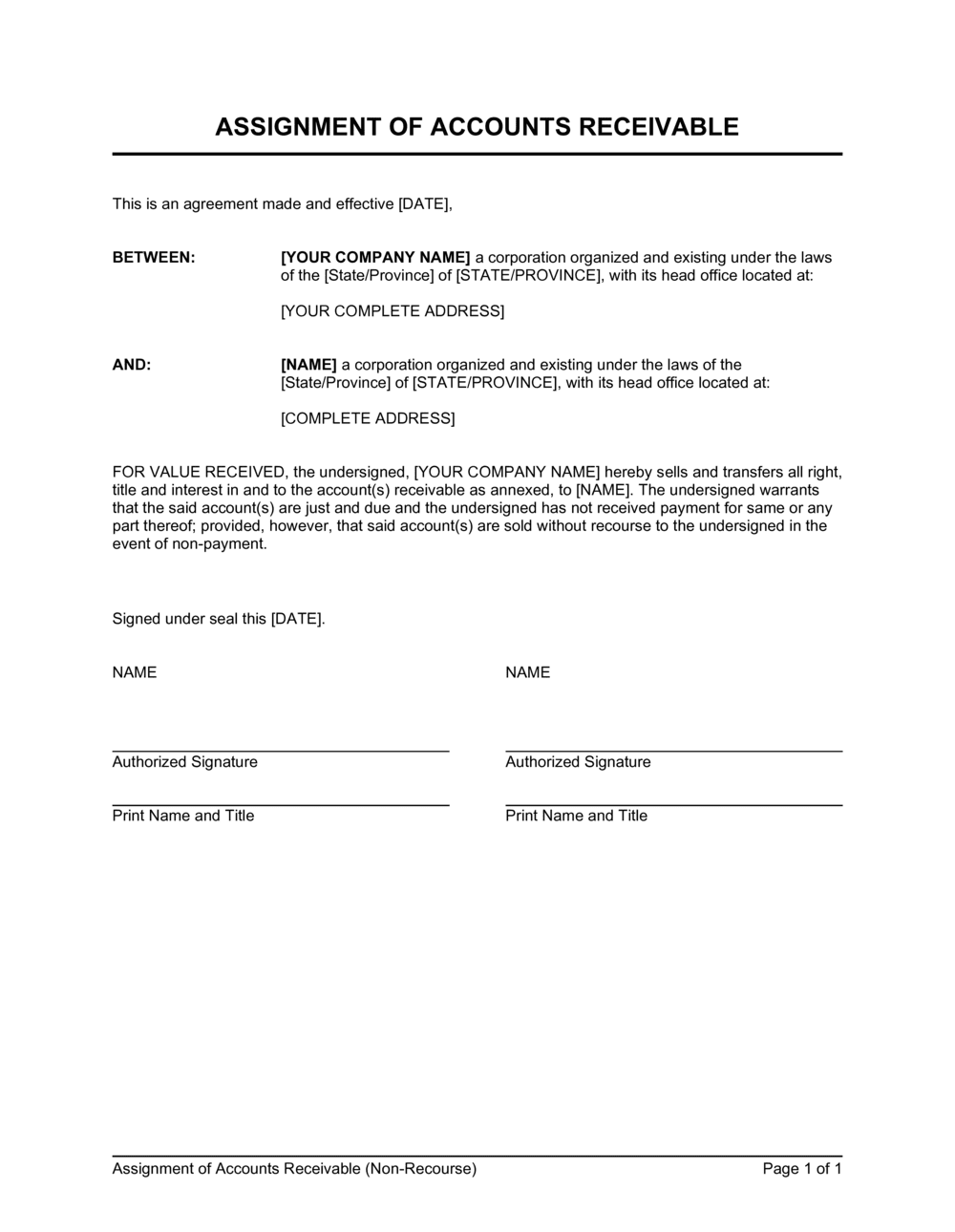

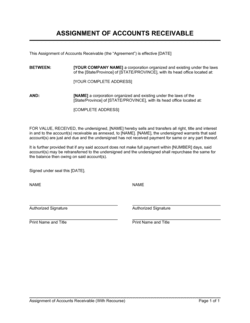

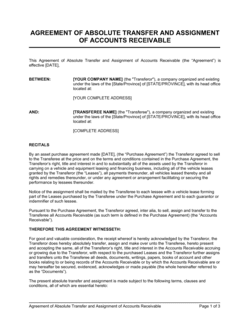

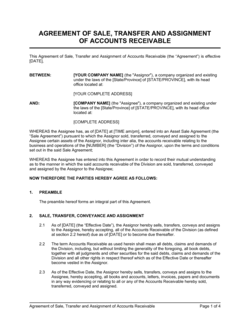

1

Identify the parties with full legal names

Enter the Assignor's and Assignee's complete registered legal names, jurisdiction of formation, entity type, and principal addresses. Confirm these match the names used on any UCC-1 or PPSA filings you intend to make.

💡 Run a quick corporate registry search before signing to confirm the exact legal name — a one-word mismatch in a UCC filing can subordinate your priority to a later creditor.

2

Complete Schedule A with every assigned receivable

List each invoice by number, the account debtor's full legal name, the face amount, the invoice date, and the due date. Attach this schedule to the executed agreement and initial each page.

💡 For ongoing factoring facilities, use a master schedule format that can be updated with each advance rather than amending the core agreement every time.

3

Set the purchase price, advance rate, and reserve terms

Enter the agreed advance rate as a percentage of face value, calculate the dollar amount payable at closing, and specify the reserve holdback percentage and the conditions and timeline for its release.

💡 Tie reserve release to a specific trigger — debtor payment confirmed in cleared funds — not to a date. Date-based release gives the Assignee no protection against last-minute payment reversals.

4

Draft the non-recourse provision carefully

State clearly that the Assignee has no right of recourse against the Assignor for debtor non-payment due solely to the debtor's financial inability or insolvency. Enumerate any carve-outs narrowly — warranty breach, fraud, or misrepresentation only.

💡 Review each carve-out against the warranties clause. Every exception to non-recourse should map exactly to a specific warranty so the scope of Assignor liability is predictable.

5

Prepare and send the notice of assignment

Use the form in Schedule B to notify each account debtor of the transfer in writing, direct payment to the Assignee's designated account, and obtain confirmation of receipt where possible.

💡 Send the notice by a method that creates a delivery record — email with read receipt, courier with signature, or registered mail. Verbal notice is generally insufficient to cut off the debtor's right to pay the Assignor.

6

File the UCC-1 financing statement (or PPSA equivalent)

File a UCC-1 in the Assignor's state of formation (for US transactions) or a PPSA financing statement in the Assignor's province (for Canadian transactions) to perfect the Assignee's ownership interest against third-party creditors.

💡 File before or simultaneously with execution, not after. A gap between signing and filing creates a window during which a judgment creditor or trustee in bankruptcy could claim priority.

7

Execute with authorized signatures before funding

Both parties must sign before the Assignee advances any funds. Ensure signatories have authority under their respective corporate governance documents — minutes, resolutions, or incumbency certificates if required.

💡 For corporate parties, attach a board resolution or officer's certificate confirming signing authority. Challenges to authority are a common tactic in assignment disputes.

8

Store the executed agreement and filing confirmations together

Keep the fully executed agreement, Schedule A, the notice of assignment, proof of debtor notification, and the UCC-1 or PPSA filing confirmation in a single organized file for each transaction.

💡 If the Assignor enters bankruptcy, the Assignee will need to produce all four documents to the trustee quickly — disorganized records can delay enforcement by weeks.