1

Gather three months of financial statements

Collect bank statements, pay stubs, tax returns, credit card statements, and loan statements for the prior three months. Using a three-month average smooths seasonal or irregular expenses and produces a more defensible budget in any legal context.

💡 Download statements directly from each financial institution rather than relying on memory — discrepancies between stated and actual figures are the most common reason family budgets are challenged in mediation.

2

Complete the household composition section

Enter the full legal names of both parties, current address, and the names and ages of all dependents. Accuracy here directly affects child support calculations, benefit eligibility assessments, and tax filing status.

💡 If a dependent is shared between two households, note the custody split percentage — many support calculations require this detail.

3

Enter all income sources at the net monthly level

List every income source for each household member — employment wages, freelance income, rental income, pension, child support received, and government benefits — using the net (after-tax) monthly figure. Label clearly whether each amount is gross or net.

💡 For irregular income (freelance, commission, seasonal), calculate a 12-month annual total and divide by 12 to produce a reliable monthly average.

4

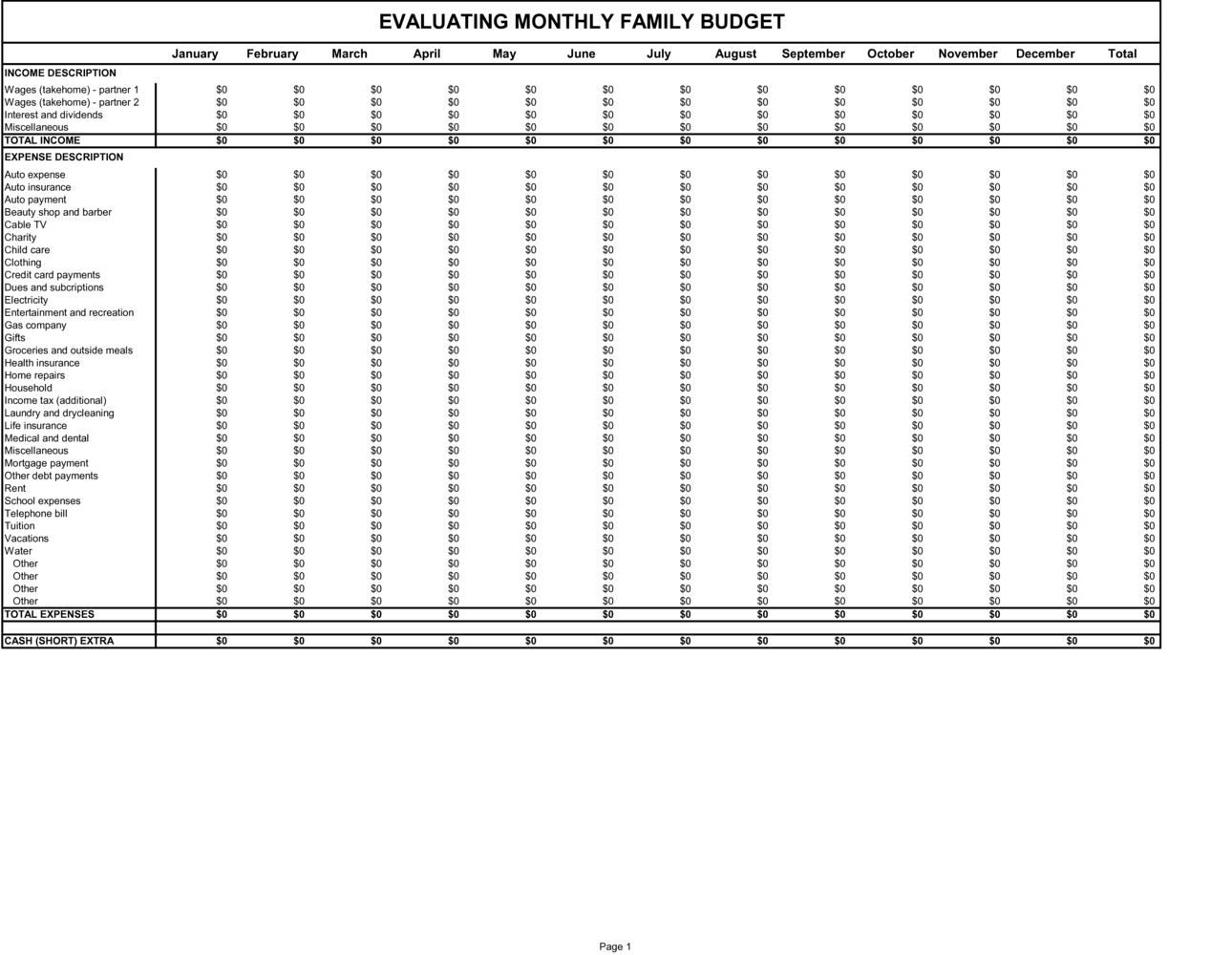

Itemize fixed expenses individually

List every fixed monthly obligation on its own line with the exact payment amount. Do not combine separate obligations — mortgage and property tax, or auto loan and auto insurance — into a single line.

💡 Pull exact amounts from statements rather than rounding. A $12 rounding difference per line across 15 lines creates a $180/month discrepancy that will be flagged in any professional review.

5

Estimate variable expenses using three-month averages

For each variable category, total the actual spending over three months from bank and credit card statements and divide by three. Record the category average in the template.

💡 Annual expenses such as vehicle registration or holiday spending should be divided by 12 and included as a monthly line item — omitting them understates real annual cash outflow.

6

Complete the debt schedule with current balances

For each debt, enter the creditor name, account type, current balance as of the document date, interest rate, and the actual monthly payment being made (not just the minimum).

💡 Order debts from highest interest rate to lowest — this layout helps a financial advisor or attorney quickly identify which obligations are most costly and prioritize repayment or negotiation.

7

Record savings and retirement contributions

Enter monthly contributions to all savings vehicles — emergency fund, 401(k), IRA, RESP, 529, and any other systematic savings — as separate line items. Pre-tax contributions should be noted as such.

💡 If savings contributions are irregular, use the annual total divided by 12. Omitting retirement contributions is the most common gap in family budget documents submitted in divorce proceedings.

8

Calculate the net surplus or deficit and obtain signatures

Total all expense and savings rows, subtract from net monthly income, and record the result. Both parties should then review the completed document, confirm accuracy, and sign the attestation and signature blocks before any legal or financial filing.

💡 If the document will be used in court, mediation, or a bankruptcy filing, have both signatures witnessed or notarized — the additional authentication step significantly increases evidentiary weight.