- Board Resolution

- A formal written decision adopted by a board of directors, recorded in the minute book, that authorizes or directs a specific corporate action.

- Quorum

- The minimum number of directors who must be present at a meeting for the board's decisions to be legally valid, as specified in the company's bylaws.

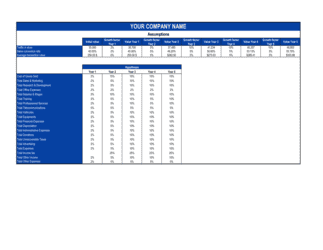

- Operating Budget

- A financial plan projecting revenues and day-to-day expenses — salaries, rent, marketing, and overheads — for a defined fiscal period, typically 12 months.

- Capital Budget

- A plan authorizing expenditures on long-term assets such as equipment, technology infrastructure, or property that will be capitalized on the balance sheet.

- Fiscal Year

- The 12-month accounting period a company uses for financial reporting, which may or may not align with the calendar year.

- Delegated Authority

- The spending limit up to which a named officer or manager may commit company funds without returning to the board for a separate resolution.

- Variance Threshold

- The maximum percentage or dollar amount by which actual spending may exceed a budget line before requiring board notification or a formal amendment.

- Recitals

- The introductory 'whereas' clauses in a resolution that provide the factual background — meeting date, attendees, and authority — supporting the decisions that follow.

- Minute Book

- The official corporate record maintained by the corporate secretary containing all board and shareholder resolutions, meeting minutes, and governance documents.

- Unanimous Written Consent

- A procedure allowing all directors to adopt a resolution by signing a written document, without holding a formal meeting, when permitted by the jurisdiction's corporate statute.

- Certification

- A statement signed by the corporate secretary or an officer confirming that the resolution was duly adopted and accurately reflects the board's vote.