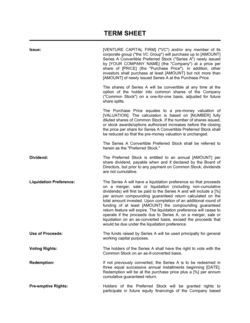

- Capitalization Table

- A record of all equity ownership in a company, showing each holder's security type, share count, and percentage ownership.

- Fully Diluted Shares

- The total share count including all issued shares plus all securities that could convert to shares — options, warrants, convertible notes, and SAFEs.

- Pre-Money Valuation

- The agreed value of the company before a new investment round is added, used to calculate the price per share for incoming investors.

- Post-Money Valuation

- The company's value immediately after a new investment is closed — calculated as pre-money valuation plus the new capital invested.

- Option Pool

- A block of shares reserved for future grants to employees, advisors, and consultants, typically sized at 10–20% of fully diluted shares before a financing round.

- SAFE (Simple Agreement for Future Equity)

- A convertible instrument that grants the right to receive equity in a future priced round, typically at a discount or valuation cap, without accruing interest.

- Anti-Dilution Provision

- A right granted to preferred shareholders that adjusts their conversion price downward if the company later issues shares at a lower price, protecting against value loss.

- Liquidation Preference

- A right that entitles preferred shareholders to receive a specified multiple of their investment before common shareholders receive any proceeds on exit.

- Pro-Rata Rights

- A contractual right allowing existing investors to participate in future funding rounds to maintain their ownership percentage.

- Vesting Schedule

- A timeline — typically 4 years with a 1-year cliff — over which a founder or employee earns the right to their equity grant.

- 409A Valuation

- An independent appraisal of a private company's common stock fair market value, required by US tax law to set legally compliant option strike prices.

- Waterfall Analysis

- A model showing how exit proceeds are distributed among shareholders in priority order — liquidation preferences first, then participation rights, then common shares.