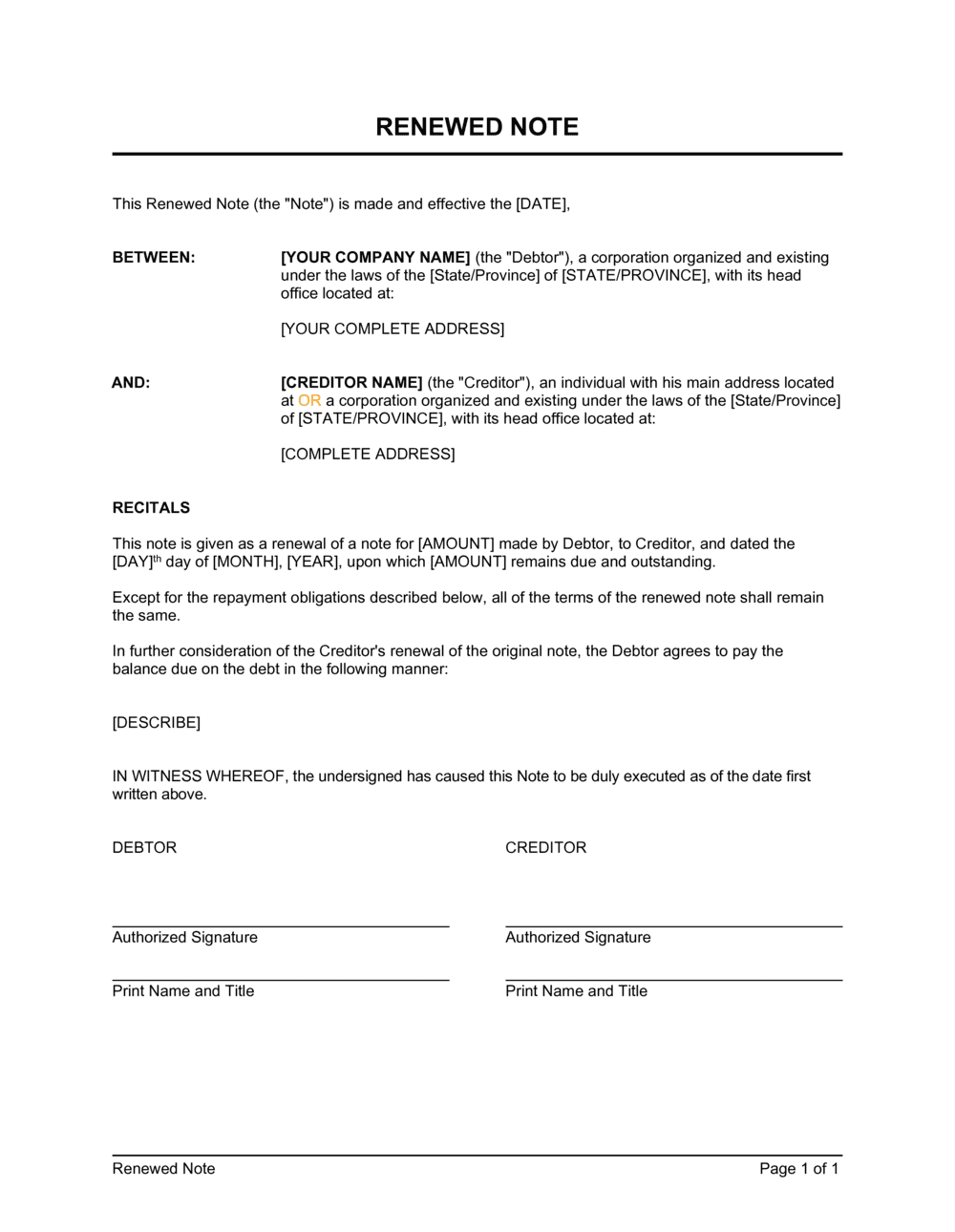

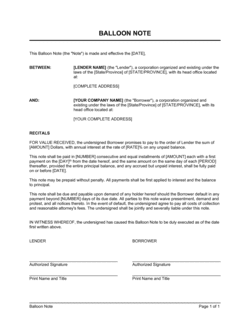

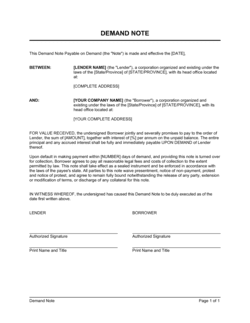

1

Gather the original note and payment history

Locate the executed original promissory note and compile a complete record of all payments received to date. You will need the original principal amount, the original execution date, and the exact outstanding balance as of the renewal date.

💡 Reconcile the payment history before you fill in the outstanding balance — a discrepancy discovered after signing requires a corrective amendment.

2

Identify both parties with their legal names

Enter the borrower and lender's full legal names exactly as they appear on the original note. For entities, use the registered corporate or LLC name, not a trade name.

💡 If either party has changed its legal name since the original note was signed, add a recital acknowledging the name change — e.g., 'formerly known as [PRIOR NAME].'

3

State the outstanding principal balance

Enter the actual remaining principal balance as of the renewal date, after crediting all prior payments. Do not use the original face amount unless no payments have been made.

💡 Have both parties sign off on the outstanding balance figure before executing the renewed note. A separate balance confirmation letter prevents disputes later.

4

Set the new maturity date

Choose a specific calendar date — not a period like 'six months from signing' — and enter it as the new maturity date. Confirm the new term is commercially reasonable and that the borrower has a realistic path to repayment.

💡 Avoid setting a maturity date that falls on a weekend or public holiday. Add language providing that if the maturity date falls on a non-business day, payment is due on the next business day.

5

Set and verify the interest rate

Enter the applicable interest rate and confirm it does not exceed the usury ceiling in the governing jurisdiction. If the rate is changing from the original note, state clearly that the new rate replaces the old one.

💡 US state usury limits vary widely — from no limit in some states to 10–16% on commercial notes in others. Check the current limit for the governing state before executing.

6

Define the revised repayment schedule

Specify payment amounts, frequency, and due dates for the renewed term. If the note will end with a balloon payment, state the balloon amount explicitly or define it as the full remaining outstanding balance on the maturity date.

💡 Include a payment application waterfall — e.g., 'payments shall be applied first to accrued interest, then to outstanding principal' — to prevent disputes on how partial payments are credited.

7

Confirm continuation of collateral and guarantees

If the original note was secured by collateral or backed by a personal guarantee, confirm in the no-novation clause that these continue to apply under the renewed note. Obtain a written reaffirmation from any guarantor.

💡 If the collateral is real property, check whether the governing jurisdiction requires the renewal to be recorded in the same registry as the original security instrument.

8

Execute with proper signatures and retain originals

Have both parties sign and date the renewed note. For entity borrowers or lenders, ensure the signatory has board or operating-agreement authority to bind the entity. Retain the original signed document along with the original promissory note.

💡 Use Business in a Box eSign to create a timestamped execution record. Store the fully-executed renewed note and the original note together in BIB Drive so both are accessible if enforcement is ever needed.