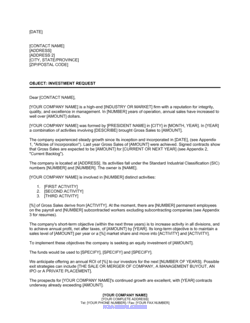

- Debenture

- A medium- to long-term debt instrument issued by a company to a lender, creating an obligation to repay principal and interest under defined terms.

- Conversion Right

- The holder's contractual option to exchange outstanding principal — and sometimes accrued interest — for shares of the issuing company at a specified price or ratio.

- Conversion Price

- The per-share price at which the debenture principal converts into equity, often set at a discount to the most recent round or pegged to a valuation cap.

- Participation Right

- A provision entitling the debenture holder to receive a share of the company's profits, revenue, or distributable cash above a defined threshold, in addition to interest.

- Mezzanine Financing

- A hybrid capital layer ranking below senior secured debt but above equity, combining debt repayment terms with equity-linked returns such as warrants or conversion features.

- Anti-Dilution Provision

- A clause adjusting the conversion price downward if the company issues shares at a lower price after the debenture is issued, protecting the holder against dilution.

- Security Interest

- A lender's legal claim over specific company assets — or all assets — as collateral, giving the holder priority recovery rights if the company defaults.

- Negative Covenant

- A contractual restriction preventing the issuer from taking specified actions — such as incurring additional debt, paying dividends, or selling key assets — without the holder's consent.

- Event of Default

- A defined trigger — such as missed interest payment, insolvency, or breach of covenant — that entitles the holder to demand immediate repayment or exercise conversion rights.

- Maturity Date

- The date on which all outstanding principal and accrued interest become due and payable if the holder has not previously exercised their conversion right.

- Subordination

- An agreement ranking the debenture holder's claims below those of senior secured lenders, defining the order of repayment in a liquidation or restructuring.

- Accrued Interest

- Interest that has accumulated on the outstanding principal since the last payment date but has not yet been paid to the holder.