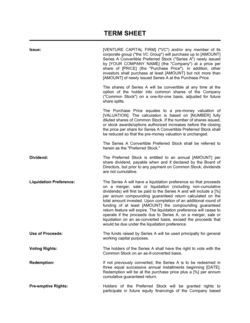

- Promissory Note

- A written instrument in which the issuer unconditionally promises to pay a specified sum to the note holder at a defined time or on demand.

- Principal Amount

- The face value of the note — the original sum borrowed or purchased — on which interest accrues.

- Maturity Date

- The date on which the outstanding principal and any accrued, unpaid interest become due and payable in full.

- Coupon Rate

- The annual interest rate stated on the note, expressed as a percentage of the principal, determining periodic interest payments.

- Accrued Interest

- Interest that has accumulated on the principal balance since the last payment date but has not yet been paid to the note holder.

- Event of Default

- A specified condition — such as missed payment, insolvency, or breach of covenant — that gives the note holder the right to accelerate repayment and pursue remedies.

- Acceleration Clause

- A provision that makes the entire outstanding balance immediately due and payable upon the occurrence of an event of default.

- Representations and Warranties

- Factual statements made by each party at closing that confirm legal authority, accuracy of disclosed information, and absence of undisclosed liabilities.

- Covenant

- A contractual obligation — either to take a specific action (affirmative covenant) or to refrain from one (negative covenant) — that the issuer must observe for the life of the note.

- Conversion Feature

- A provision in a convertible note allowing the holder to exchange the outstanding balance for equity at a defined price or discount, typically triggered by a qualifying financing event.

- Subordination

- An agreement by a junior note holder to rank their repayment claim below that of senior creditors in the event of liquidation or default.

- Valuation Cap

- A ceiling on the company valuation used to calculate the conversion price for a convertible note, protecting early investors from excessive dilution.