- Inherent Risk

- The level of risk present before any controls or mitigation measures are applied.

- Residual Risk

- The risk that remains after controls have been implemented — the exposure the organization chooses to accept or monitor.

- Risk Appetite

- The total amount and type of risk an organization is willing to accept in pursuit of its strategic objectives.

- Risk Tolerance

- The acceptable variation around a specific risk target — a narrower operational boundary within the broader risk appetite.

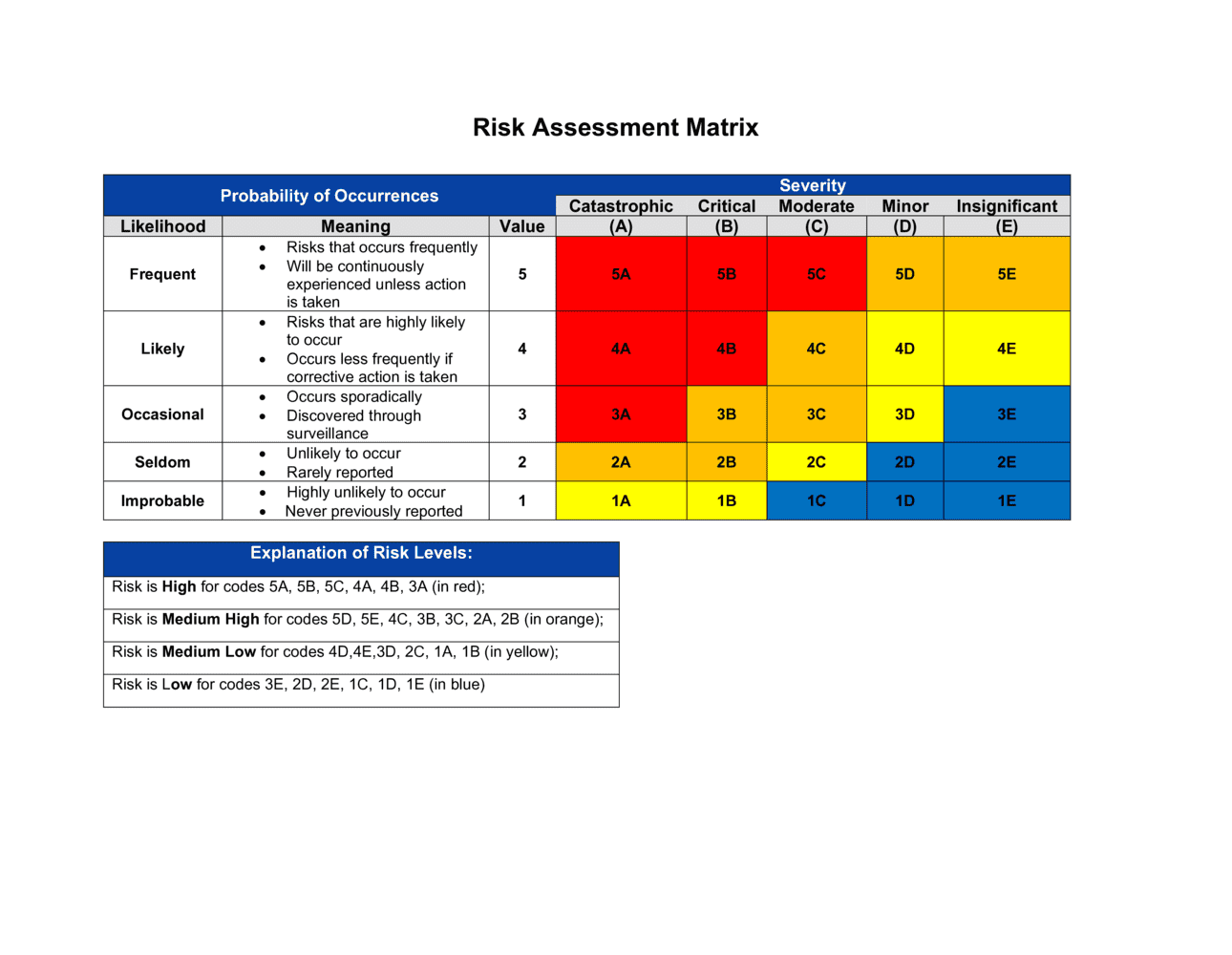

- Likelihood Score

- A numeric rating (typically 1–5) estimating the probability that a given risk event will occur within the assessment period.

- Impact Score

- A numeric rating (typically 1–5) estimating the severity of consequences if a risk event occurs — covering financial, operational, reputational, or legal harm.

- Risk Priority Rating

- The product of Likelihood Score multiplied by Impact Score, used to rank risks and determine the urgency of mitigation action.

- Mitigation Control

- A specific action, policy, system, or safeguard designed to reduce the likelihood or impact of an identified risk.

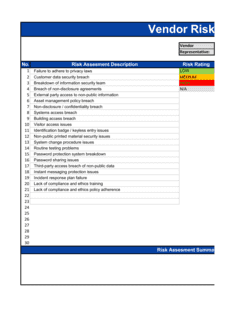

- Risk Owner

- The named individual accountable for monitoring a specific risk, implementing assigned controls, and reporting on residual exposure.

- Risk Register

- A complete log of all identified risks, their scores, owners, controls, and review dates — the Risk Assessment Matrix is the structured analytical layer on top of the register.

- Control Effectiveness

- An assessment of how well an existing mitigation measure actually reduces the identified risk, rated on a scale from ineffective to fully effective.

- Risk Treatment

- The chosen strategy for handling a risk: avoid it, reduce it, transfer it (e.g., via insurance), or accept it with documented rationale.