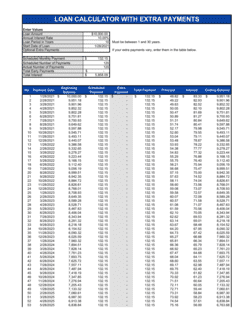

❌ Framing the deferral as a waiver or forgiveness

Why it matters: Language that implies the December payment is forgiven rather than deferred can extinguish the lender's right to collect it, creating an unintended write-off and a tax event.

Fix: Use explicit loan-offer language confirming the deferred amount remains outstanding and will be repaid with accrued interest on the new due date.