1

Identify both parties with full legal names and addresses

Enter the payer's and payee's registered legal names — not trade names — and current mailing addresses. If either party is an entity, include the entity type and state of incorporation.

💡 For sole proprietors, use the individual's full legal name as it appears on their government-issued ID to avoid enforceability questions.

2

State the total amount owed and its origin

Enter the exact principal balance and describe in one sentence where the debt came from — unpaid invoice, prior loan, service rendered, or settlement of a dispute.

💡 Reference any underlying invoice number, contract, or account number so the agreement connects clearly to the originating obligation.

3

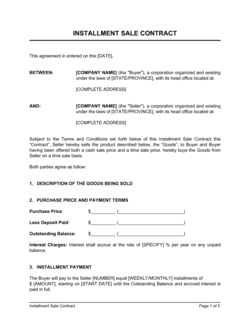

Build the payment schedule with specific dates

List each installment amount and its calendar due date. Do not use vague terms like 'monthly' — use exact dates (e.g., the 1st of each month beginning June 1, 2026). Attach an amortization table as Schedule A if interest is included.

💡 For agreements with interest, use an online amortization calculator to generate the table before filling in the schedule — manual calculations frequently contain rounding errors that compound over time.

4

Set the interest rate and verify the usury limit

Enter the annual interest rate and confirm it does not exceed the statutory maximum in the governing jurisdiction. Consumer agreements and commercial agreements typically have different caps.

💡 In the US, usury limits vary from 6% to 45% depending on the state and transaction type. Look up the applicable limit before signing — exceeding it can void the interest obligation entirely.

5

Define the grace period and late fee

Enter a grace period of 5–10 calendar days and a late fee that is proportionate to the installment amount. A fee equal to 1.5–5% of the overdue installment is generally enforceable in most jurisdictions.

💡 Keep the late fee below 10% of any single installment and document it as a reasonable estimate of collection costs, not a penalty — this framing strengthens enforceability.

6

Include the acceleration clause and default triggers

Confirm the default triggers cover at minimum: missed payment beyond the grace period, insolvency, and bankruptcy filing. Ensure the acceleration clause allows the full balance to be called immediately on default without requiring additional notice.

💡 Add a cross-default clause if the payer has other agreements with you — a default on one agreement triggers default on all, preventing a payer from selectively honoring some obligations while ignoring others.

7

Decide on collateral and file the UCC-1 if applicable

If the agreement is secured, describe the collateral with sufficient specificity to identify the asset — serial numbers, VINs, or account numbers where applicable. Plan to file a UCC-1 financing statement with the appropriate state office within 10 days of signing.

💡 Unsecured payment agreements are faster to execute but rank behind secured creditors in a bankruptcy. For obligations above $5,000, the filing fee for a UCC-1 is typically under $25 and significantly strengthens your position.

8

Execute before any payment is accepted

Both parties must sign the agreement before — or simultaneously with — the first installment payment. Accepting a payment before signing can be interpreted as ratifying an oral arrangement on less favorable terms.

💡 Use timestamped electronic signatures and retain an executed copy in a secure document folder accessible to both parties.