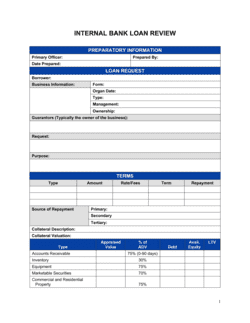

1

Enter the applicant's legal entity details

Fill in the borrower's full registered legal name, address, and primary contact. Cross-reference the original application to confirm the name matches incorporation documents.

💡 For business applicants, include both the legal entity name and the operating trade name if they differ, to prevent processing delays.

2

Record the application reference number and original date

Enter the unique reference number assigned to the financing application at submission. This links the approbation to every document in the credit file.

💡 Use a consistent numbering format — APP-YYYY-NNNN — so approbations can be sorted and retrieved by year without a database query.

3

State the approved amount, currency, and purpose

Enter the exact approved dollar amount in the applicable currency. Describe the financing purpose in enough detail to distinguish it from other facilities the borrower may hold.

💡 If the approved amount differs from the amount requested, note both figures and add a brief explanation — this prevents borrower confusion and potential disputes.

4

Specify the interest rate, fee structure, and rate type

Enter the annual interest rate, state whether it is fixed or variable, and list all fees. For variable rates, name the reference index (e.g., Prime + 2%) and any rate cap.

💡 Express the effective APR in addition to the nominal rate — it gives borrowers and auditors a single comparable figure.

5

Define repayment terms with specific dates and amounts

Enter the loan term in months, payment frequency, installment amount, and the exact maturity date. Calculate the installment amount before filling it in — do not leave it as a formula placeholder.

💡 Include the first payment due date explicitly; many borrowers assume a 30-day grace period that does not exist.

6

Describe collateral with identifying details

List each pledged asset by make, model, serial number or VIN, and estimated value. Note the lender's lien position if other creditors have prior claims on the asset.

💡 Attach a separate collateral schedule as an appendix for complex multi-asset security packages rather than cramming all details into the form body.

7

List conditions of approval as measurable obligations

Write each condition as a specific, verifiable action with a deadline — avoid open-ended language. Distinguish between conditions precedent to disbursement and ongoing covenants.

💡 Number each condition and leave a checkbox column so the lending officer can tick off each one as it is satisfied before releasing funds.

8

Complete the authorization block and file the document

Enter the approver's printed name, title, department or committee, and the exact approval date. File the signed original in the credit file and send a copy to the borrower.

💡 Date-stamp the document at the time of filing — approval date and file date sometimes differ, and both matter for compliance purposes.