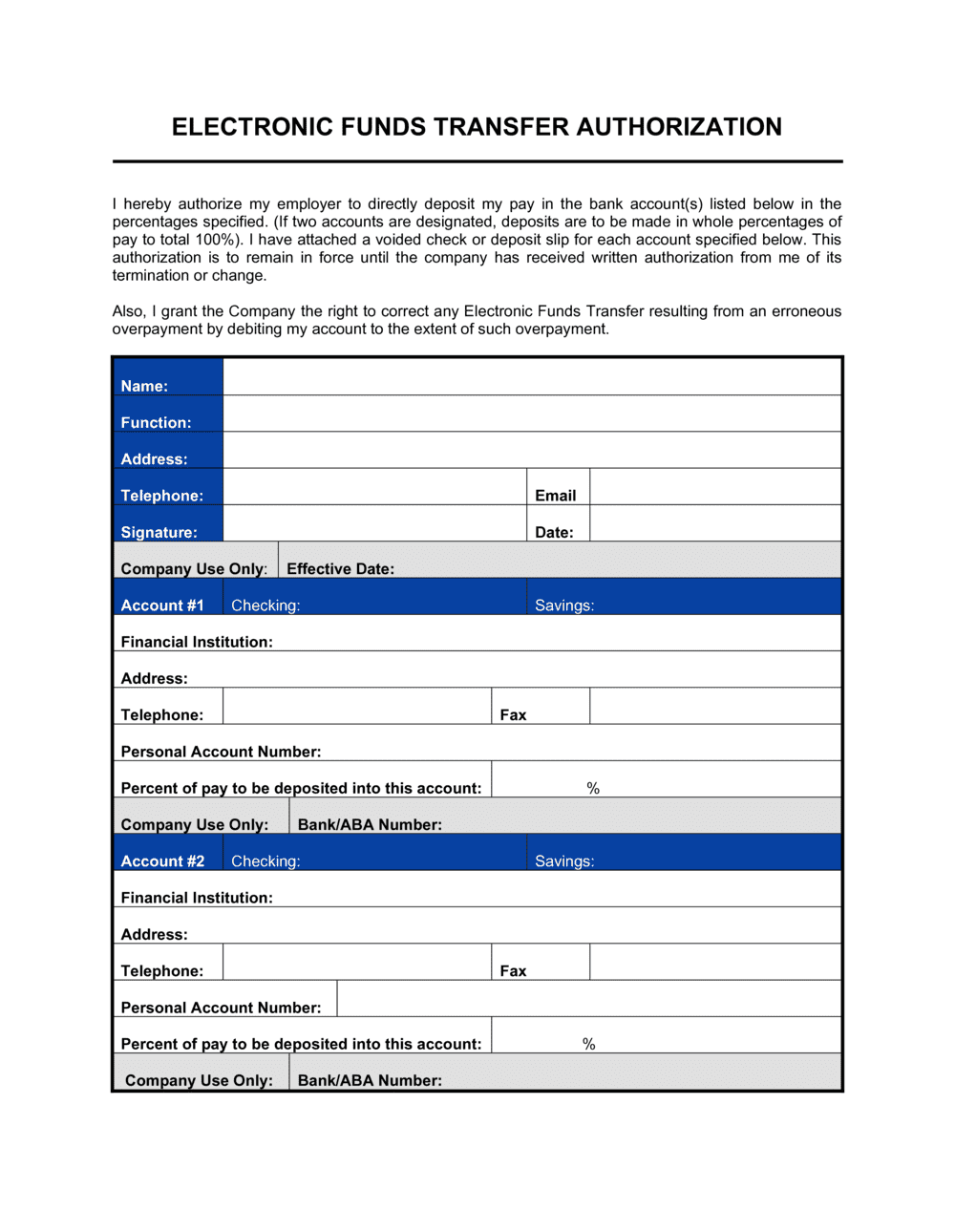

- ACH Transfer

- Automated Clearing House transfer — the electronic network used to move funds directly between bank accounts in the United States.

- Routing Number

- A nine-digit number that identifies a specific financial institution within the ACH network, printed at the bottom-left of a check.

- Account Number

- A unique number assigned to an individual bank account, used with the routing number to direct funds to the correct destination.

- Prenote

- A zero-dollar test transaction sent through the ACH network before the first live deposit to verify that the routing and account numbers are valid.

- Voided Check

- A check with 'VOID' written across it, submitted alongside an enrollment form to confirm routing and account numbers without allowing funds to be drawn.

- Deposit Allocation

- Instructions specifying what portion of a paycheck goes to each account when an employee designates multiple bank accounts.

- Net Pay

- The amount deposited after all taxes, deductions, and withholdings have been subtracted from gross wages.

- Preauthorized Debit

- Written permission allowing a company to withdraw funds from an employee's or customer's account, required for ACH compliance.

- RDFI (Receiving Depository Financial Institution)

- The employee's bank or credit union that receives the direct deposit funds through the ACH network.

- EFT (Electronic Funds Transfer)

- The broad category of digital money movement that includes direct deposit, wire transfers, and ACH transactions.