1

Insert the corporation's full legal name and jurisdiction

Enter the exact registered name of the corporation — including 'Inc.', 'LLC', 'Ltd.', or equivalent — and the state, province, or country of incorporation. Cross-reference the articles of incorporation or certificate of formation to confirm the name is spelled identically.

💡 Request a certified copy of your articles from the state registry if you are unsure of the exact registered name — banks will reject mismatched names.

2

Confirm the method of adoption — meeting or written consent

Indicate whether the resolution was passed at a duly noticed board meeting with quorum confirmed, or by unanimous written consent in lieu of a meeting. Both methods are valid in most jurisdictions, but the recitals must reflect the correct procedure.

💡 Written consent resolutions require the signature of every director in most US states — check your bylaws before choosing this method.

3

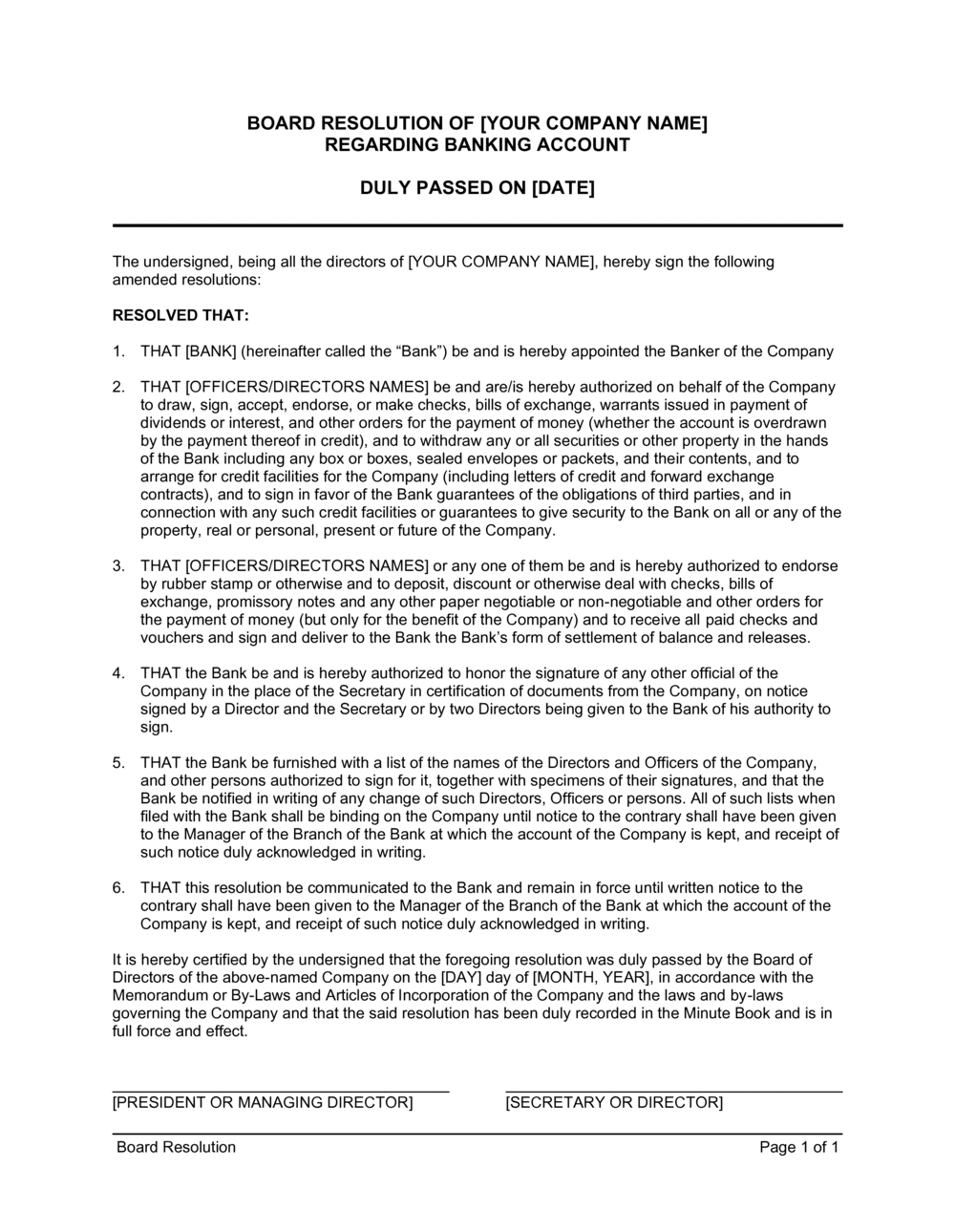

Name the specific bank and account type

Insert the bank's full legal name (e.g., 'JPMorgan Chase Bank, N.A.') and the type of account being authorized (e.g., business checking, money market, or line of credit). If opening multiple accounts, list each on a separate resolution or add separate 'RESOLVED FURTHER' clauses.

💡 Call the bank's business banking team before finalizing to confirm whether they have a preferred resolution format — some large banks supply their own form.

4

List each authorized signatory with full name, title, and transaction limits

Enter the legal name and current title of every officer or employee who will have signing authority. If dual control is required above a certain dollar threshold, state it explicitly (e.g., 'any two of the foregoing for transactions exceeding $10,000').

💡 Keep the signatory list as short as operationally necessary — each additional signatory is a potential fraud vector and a future amendment obligation when personnel change.

5

Enumerate the scope of banking powers

List every action the signatories are authorized to perform: check signing, wire transfers, ACH initiation, online banking access, overdraft authorization, and execution of loan documents. Omitting an action type means signatories technically lack authority for it.

💡 Include online banking and mobile banking explicitly — many resolutions predate these channels and leave electronic access in a legal grey area.

6

Obtain specimen signatures from each authorized signatory

Have each listed signatory sign their name in the specimen signature block — not a printed name, not initials. The bank will store this as the verification baseline for future transactions.

💡 If a signatory uses a different signature for banking than for other documents, note that and ensure the banking signature is used consistently.

7

Have the corporate secretary certify and date the resolution

The secretary — someone who is not themselves an authorized signatory — signs the certification block, confirms the adoption date, and attests that the resolution is current and unrescinded.

💡 Keep a certified copy in the corporate minute book and provide the bank with a separate certified copy stamped 'Certified True Copy' on each page.

8

Submit to the bank and confirm acceptance

Deliver the certified resolution to the bank's business banking officer before or at account opening. Confirm in writing that the bank has updated its records — do not assume the resolution is on file until you receive written confirmation.

💡 Request a signed acknowledgment from the bank confirming receipt and acceptance of the resolution — this protects you if a future transaction is disputed on authorization grounds.