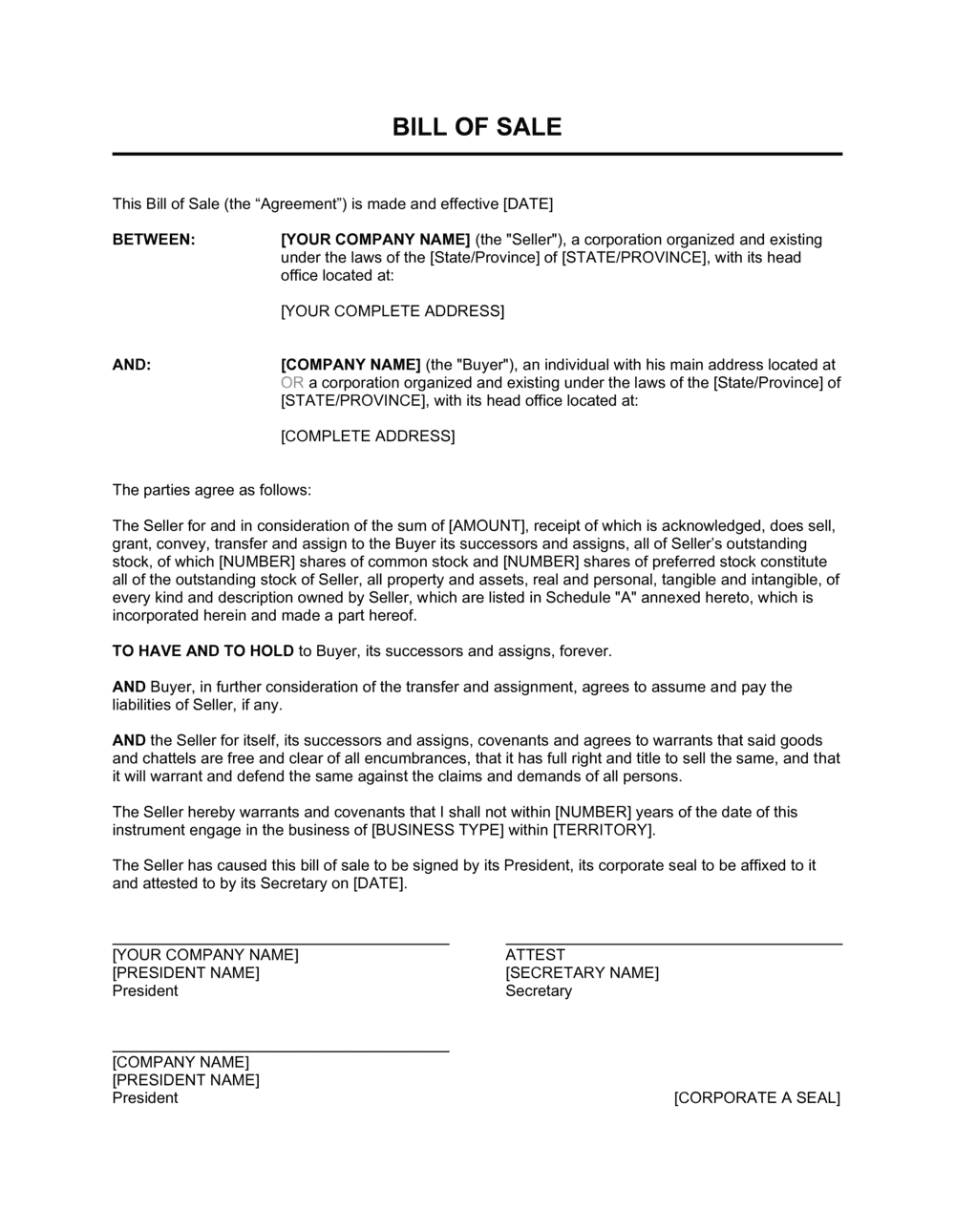

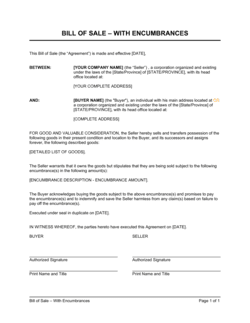

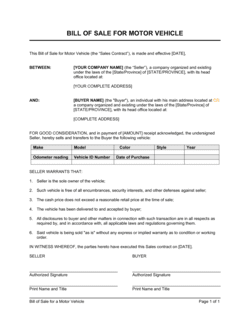

1

Identify both corporations by full legal name

Enter the seller's and buyer's complete registered corporate names exactly as they appear in their respective state or provincial corporate registry filings. Include the state or jurisdiction of incorporation and principal address for each.

💡 Pull the exact legal name from a current certificate of good standing, not from a business card, website, or letterhead — trade names frequently differ from registered names.

2

Describe each asset with serial-level specificity

For each asset being transferred, provide the full name, make and model, serial number or VIN, year of manufacture, and current physical location. If transferring multiple assets, use a numbered Schedule A attached to the agreement.

💡 Photograph each asset on the closing date and attach the images to the executed file — this record eliminates condition disputes months later.

3

State the purchase price and payment method

Enter the total consideration in both numerals and written words. Specify whether payment is by wire transfer, certified check, or ACH, and confirm the date by which payment must be received.

💡 For intercompany transfers at nominal consideration (e.g., $1), document the business reason in a board resolution or memo to support the transfer at the stated price for tax and accounting purposes.

4

Confirm title and search for existing liens

Before executing, run a UCC lien search against the seller in the relevant secretary of state's office and confirm that no financing statements are filed against the asset. If liens exist, arrange for payoff and lien termination filings prior to or simultaneously with closing.

💡 A UCC-3 termination statement filed by the secured party — not just a payoff letter — is required to clear a lien from public records.

5

Select the appropriate condition and warranty language

Decide whether the asset is sold as-is with no warranty or with a limited warranty of condition. If as-is, present the disclaimer in uppercase to meet conspicuousness requirements in most US states. If warranting condition, specify exactly what is warranted and for how long.

💡 For high-value assets sold as-is, obtain a signed buyer acknowledgment that they inspected the asset prior to purchase — this reduces post-sale claims significantly.

6

Tailor representations and add an indemnification cap

Review each representation and warranty against what you actually know about the asset. Delete or qualify any statement you cannot confirm. Add an explicit indemnification liability cap — typically 100% of the purchase price — to limit post-closing exposure.

💡 Survival periods for representations should match the relevant statute of limitations in the governing jurisdiction, typically 2–4 years.

7

Obtain a corporate resolution authorizing the sale

Before or at closing, pass a board or officer resolution authorizing the specific sale — identifying the asset, buyer, and purchase price. Attach it as an exhibit or keep it in the corporate minute book.

💡 Many buyers' counsel will require a copy of the resolution as a closing condition. Having it ready avoids last-minute delays.

8

Execute with authorized signatories and deliver originals

Have an officer with signing authority — President, CEO, or someone specifically authorized by resolution — execute on behalf of each party. Date the document on the actual signing date. Deliver a fully executed original or PDF to both parties and retain copies in each corporate records file.

💡 Use a timestamped e-signature platform to create a tamper-evident audit trail, particularly for transactions over $50,000.