There is no passion to be found playing small – in setting for a life that is less than one you are capable of living” – Nelson Mandela.

Consumers today typically have mixed or unfavorable attitudes toward marketing practices.

Whether it’s the promise of more value than can be delivered, being persuaded to buy something you don’t need, or buying unsafe, shoddy products, unsustainable marketing leads to distrust.

Marketing has been criticized for harming consumers with deceptive claims and practices and high-pressure sales. Unsustainable marketing has often fueled the desire for materialism versus quality of life. Increasing demand for more and more stuff has also led to environmental consequences.

Consumers today want a better quality of life and be more active in making the world a better place. They want to support companies – big, small, and in between – that demonstrate strong ethics and stewardship of human beings and the planet.

In fact, according to the Ethical Consumer US report of 2015 by Mintel, more than 63% of consumers feel that ethical issues are becoming more important. And consumers are strongly supporting businesses that incorporate meaningful values into their core business.

This desire to make a positive impact translates into a key concept in today’s business world: sustainability. Sustainability as a business strategy is becoming increasingly appealing to managers, executives, and business owners, and more businesses and organizations are driving change – and success – with sustainable business goals.

Here, we’ll take a close look at sustainability and how it plays out as a strategy for both business and marketing. What do sustainable businesses look like? And how can sustainable marketing help those businesses succeed?

→ Download Now: Free Business Plan Guide

Although the concept may seem new, sustainability has actually been around for decades. The modern-day concept of sustainability was developed by the World Commission on Environment and Development, an organization launched by the United Nations in 1983. The Commission was led by Norwegian Prime Minister Gro Brundtland, and thus became known as the Brundtland Commission.

After four years of work, the Commission concluded that government and industry needed to practice more environmental and social responsibility. The term sustainable development was coined and defined as:

Development that meets the needs of the present without compromising the ability of future generations to meet their own needs

Since then, sustainability in business has driven value. Harvard Business Review reports that companies that have sustainable business practices experience greater risk management, more innovation, and better financial performance, including larger profits, more cost savings, and improved efficiencies and logistics. Moreover, sustainable businesses benefit from improved customer loyalty.

According to the Clarkston Consulting 2014 Corporate Sustainability Trends Report, “sustainability has emerged to a prominent position in corporate and consumer consciences.”

Among the consumers who are noticing the movement toward sustainability are millennials, who now boast $2.45 trillion in spending power. Forbes reports millennials not only have money to spend, they care where they spend it: roughly 70% will pay more for brands that support a cause they care about.

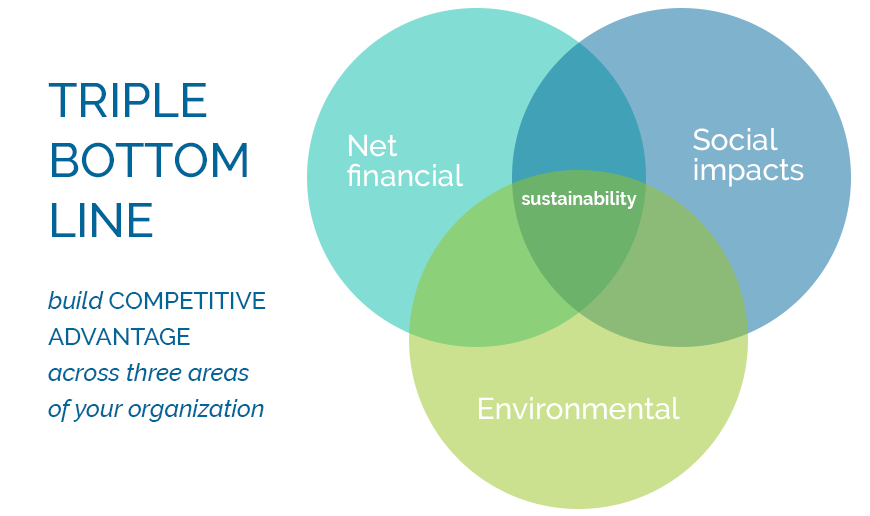

As the purchasing power of millennials increases and the population of conscientious consumers continues to grow, authentically sustainable, purpose-driven brands and the people-planet-profit model are winning across the board – economically and socially.

- Net financial

- Environmental

- Social impacts

A crucial element of this approach is to broaden the consideration of stakeholders beyond shareholders to all groups that have an interest in and are impacted by the organization.

Several companies have embraced best practices of sustainable business with success. Patagonia and Interface are two that have created sustainable solutions while differentiating their brands and winning consumer loyalty.

Patagonia

Patagonia founder Yves Chouinard brought his love of the outdoors, concern for the planet, and passion for sports together in a company that supplies the world’s top climbers, fishermen, surfers, and outdoor enthusiasts with high-quality gear. To be successful and profitable, the company has built its mission on sustainable sourcing, supply chain innovation, and valuing relationships with vendors, customers, and stakeholders.

Interface

After starting his business in the 1970s, carpet manufacturer Ray Anderson realized it was contributing to pollution, and he challenged his company to make carpet sustainably. In a major mid-course correction, Interface reinvented nearly every aspect of its business based on the Mission Zero goal of zero impact on the planet. With their new mission, Climate Take Back,™ the business is committed to creating a climate fit for life while calling on others to do the same.

Sustainable marketing is a critical part of operating a sustainable business. But what does the term sustainable marketing really mean?

Sustainable

Sustainable is the ability of a system to maintain or renew itself perpetually. It can also mean: conserving an ecological balance by avoiding depletion of natural resources.

The term sustainable has branched into sustainable development and sustainable business, setting the stage for sustainability to become a key indicator of an organization’s success.

“In recent years, sustainability has been recast as a broader concept encompassing the social, economic, environmental, and cultural systems needed to sustain any organization. A sustainable organization, and similarly a sustainable person, is prepared to thrive today and tomorrow.” – Adam Werbach, author of Strategy for Sustainability: A Business Manifesto

Marketing

The American Marketing Association’s definition of marketing is comprehensive, and works well toward building the definition of sustainable marketing as a multiple stakeholder approach:

Marketing is the activity, set of institutions, and processes for creating, communicating, delivering, and exchanging offerings that have value for customers, clients, partners, and society at large.

In our rapidly accelerating digital age, business leaders often lose sight of the three core functions that are needed to create value:

- Operations, which produce and deliver the product or service to the customer

- Finance, which tracks the flow and needs of capital

- Marketing, creates demand for an organization’s product or service

All of these functions are needed to build value. Without any one of them, an organization is likely to fail.

Sustainable Marketing

Here is the textbook definition of sustainable marketing, as stated in Sustainable Marketing by Diane Martin and John Schouten.

“[Sustainable marketing is the] process of creating, communicating and delivering value to customers in such a way that both natural (resources nature provides) and human (resources people provide) capital are preserved or enhanced throughout.”

Believing that marketing has “great potential as a force for creating cultural change,” Martin and Schouten set out to illustrate that marketing has two imperatives: to market sustainably and to market sustainability.

Market sustainably is an inward practice that ensures all marketing processes are environmentally and socially benign.

Market sustainability is an outward practice that helps bring about a society in which striving for sustainability is the norm.

A good way to practice sustainable marketing is to be committed to honesty in marketing messaging and sustainability claims.

Here are the five principles of sustainable marketing that you can embrace today and put to work in your organization:

- Consumer-oriented marketing

Consumer-oriented marketing means that the company or organization views its marketing strategy from the consumer’s point of view.

(We’ve already got this one covered with the inbound marketing methodology! ) - Customer value marketing

Customer value marketing entails putting most efforts and resources into continuously improving the value added to the offering. As the company creates value for the customer, the customer in turn creates value for the company. Sustainable! - Innovative marketing

The principle of innovative marketing ensures that an organization never stops finding better ways to develop products, services, and better ways to market. Those that ignore innovation will lose customers to those that find better and better ways. - Sense-of-mission marketing

Sense-of-mission marketing is the principle that guides a firm to define a broad mission that speaks to society rather than just the product. Adopting a broad mission gives a company a clear, long-term direction and serves the best long-run interests of consumers and the brand. - Societal marketing

With the principle of societal marketing, the company balances decisions based on the customer wants, the company requirements, and the customer and society’s long-term interests. For example, Method home products put the ‘hurt on dirt without doing harm to people, creatures or the planet’. Innovative companies look ahead to potential societal issues as opportunities.

Sustainable marketing goes beyond the concern for the needs and wants of today’s society, but focuses on the well-being of all stakeholders and the broader world.

In turn, this mega-trend in business is rewarded with a competitive advantage by earning the trust and loyalty of consumers. Win-win!

Manage your personal credit

Credit is the lifeblood of a small business, and you need to make sure your personal credit is also solid. Pay your bills on time. Even if money is tight and you can only afford to make a minimum payment on a credit card, it’s better to do that than to miss a payment or pay late.

Also, pay attention to your credit utilization ratio—the percentage of your available credit limits that you’re actually borrowing at any given time during the month. If you can keep this ratio below 30%, this will help you to have a better credit score and an easier time getting approved for personal loans.

Having better personal credit can also be helpful for your business, especially if your business is still establishing credit under the business’s name. And staying on top of your debt payments and due dates will help you have a stronger foundation for your personal finances.

Save for retirement

Small business owners often invest a lot of their profits back into their business, but there are also some great options for small business owners to save for retirement. Consider setting up a SEP IRA or other tax-advantaged retirement savings plan for your business, even if you don’t have any employees.

Depending on your income and qualifying factors, you may find you can save more money for retirement as a self-employed person than you could as an employee.

Instead of investing all your profits back into your business, saving for retirement can help you diversify your savings into a wider array of investment options: stocks, bonds, ETFs, and money market mutual funds. Your business is already your biggest investment. You already are depending on your business for income and insurance. You don’t have to invest every last dollar back into your business; invest in a broader range of opportunities, too.

Once you’re saving for retirement, make sure you are investing in a diversified portfolio of assets that are appropriate for your time horizon and risk tolerance. If you are still relatively young and have several decades until you reach retirement age, you should invest your portfolio mostly in stocks.

For example, an old rule of thumb for asset allocation used to be that you should take 100 minus your age, and that would be the percentage of your portfolio that should be invested in stocks. So if you were 40 years old, to calculate your portfolio, you would subtract 40 from 100, and the result would be investing 60% of your money in stocks; 40% in bonds and cash.

However, depending on your investment goals, you might want to invest an even larger percentage of your portfolio in stocks, so you can capture more of their potential long-term growth until you retire. Stocks can be risky, but they generally offer the best potential for long-term ROI.

Seek professional help

Talk to a financial adviser for more specific advice; this column does not constitute professional financial advice, but it helps to consider some of your options so you can make informed decisions about your personal finances.

If you can improve your personal finances—with a solid emergency fund, strong personal credit, and a diversified portfolio of retirement savings aside from the equity that you own in your business—you will more likely be able to focus on running your company with a mindset of calmness and optimism. And for business owners, who are some of the busiest people in the world, having peace of mind about personal finances can be truly priceless.